What changes can I expect to find in my Medicare plan's Annual Notice of Change (ANOC) letter?

Your Medicare Part D or Medicare Advantage plan can change every year and your Medicare plan is required to summarize any

plan changes in your Annual Notice of

Change letter (ANOC) that you should receive in the mail late-September or

early-October. If you have not received your plan’s ANOC letter,

please call your plan’s Member Services department and ask for another copy of the ANOC - the toll-free telephone number for Member Services can be found on your Member ID card.

What year-to-year changes can you expect in your Medicare Part D or Medicare Advantage plan?

Here are a few example:

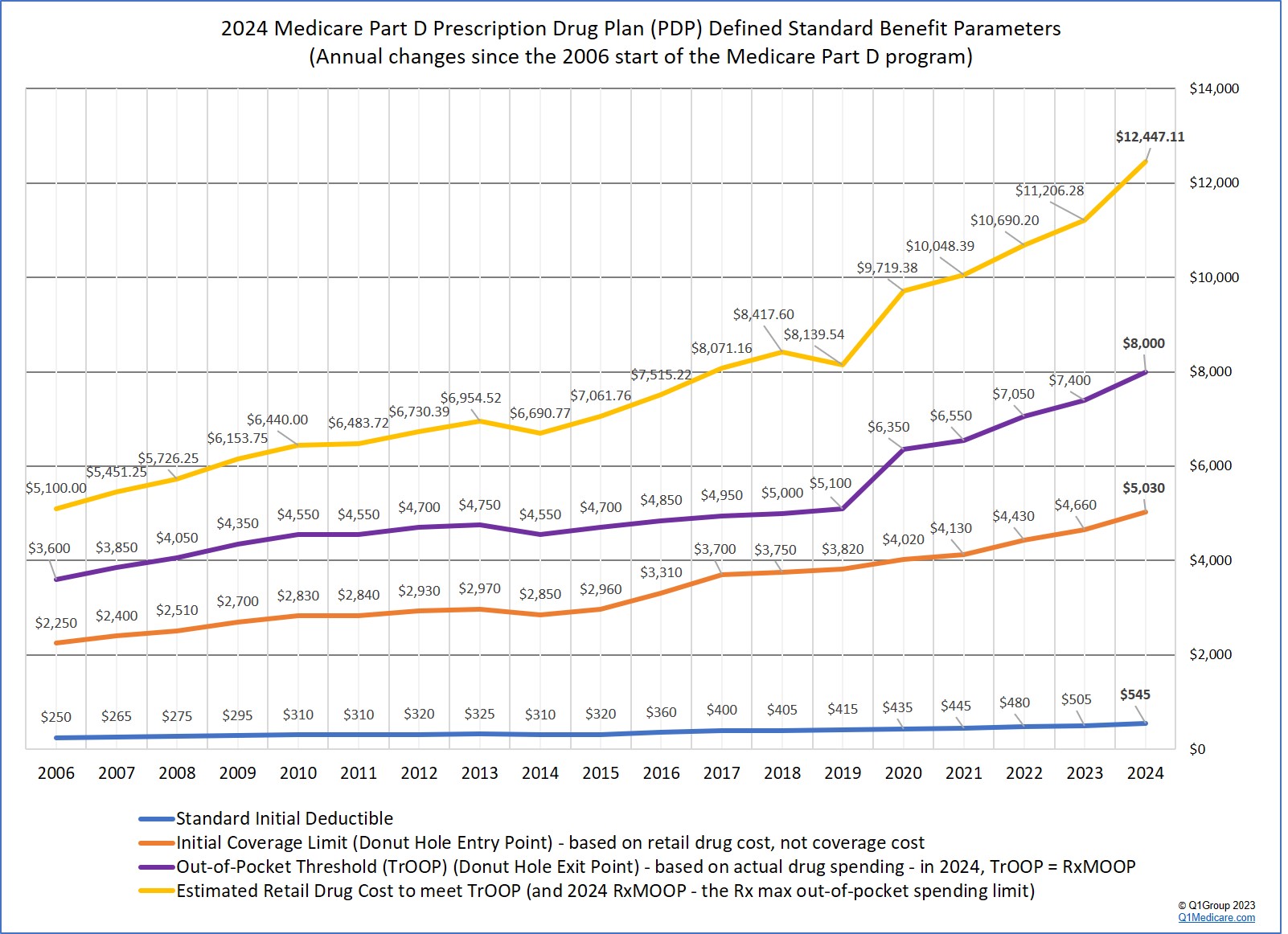

Not only can your Medicare plan change, but also the general or standard Medicare Part D prescription drug plan design will change with change to the standard deductible and initial coverage limit. Here is a chart showing how the Part D drug plans have changed over the years. Starting in 2025, Medicare Part D plans will be simplified with only an initial deductible and a $2,000 initial coverage limit that will act as the maximum out-of-pocket spending limit for formulary drugs (or RxMOOP),

What year-to-year changes can you expect in your Medicare Part D or Medicare Advantage plan?

Here are a few example:

- Monthly plan premiums can increase (or decrease) (for example, increasing from $44 to $55 per month),

- Initial drug deductibles can increase (for example, increasing from $505 to $545 in 2024),

- Initial coverage limits, for example the standard ICL is increasing from $4,660 to $5,030 in 2024. This is the maximum retail value of your medications before entering the Donut Hole when you get a 75% discount on all formulary drugs,

- Prescription drugs that are covered by your plan (the size of the plan's formulary and changes in coverage of specific brand-name and generic drugs - for example, your Tier 1 generics may be moved to Tier 2 Non-Preferred Generics),

- Drug coverage costs or cost on each formulary tier (what you pay for your drugs - such as a $5 copay or 25% coinsurance),

- Drug usage management restrictions (for example, does your drug now have a Quantity Limit or require Prior Authorization),

- Pharmacy networks (usually a Medicare drug plan will expand their pharmacy network each year and may change standard or preferred pharmacies),

- Healthcare provider networks (for Medicare Advantage plans doctors or specialists can be added - or removed from your plans "in-network" coverage),

- Copayments for medical treatment (for Medicare Advantage plans your healthcare costs can change year-to-year), and

- Your Medicare Advantage plan’s Maximum Out-of-Pocket (MOOP) spending limit for in-network, eligible Medicare Part A and Part B coverage.

Not only can your Medicare plan change, but also the general or standard Medicare Part D prescription drug plan design will change with change to the standard deductible and initial coverage limit. Here is a chart showing how the Part D drug plans have changed over the years. Starting in 2025, Medicare Part D plans will be simplified with only an initial deductible and a $2,000 initial coverage limit that will act as the maximum out-of-pocket spending limit for formulary drugs (or RxMOOP),

Important: Studies show that most people (about 70%) do not change their Medicare Part D or Medicare Advantage plan each year, even if they can save money on their prescription and medical costs - and we can appreciate that, for some people, the value of consistency outweighs the potential for savings - however, we want to remind you that, if you decide to stay with your current Medicare plan into next year, your Medicare plan coverage and costs can change, so please take time to know how your current Medicare plan is changing next year.

- How might your Medicare plan change next year and how many people will be affected by the change?

See our example for 2023: Q1News.com/978

The Good News: After receiving your ANOC letter in September or early-October, you will have plenty of time to review your Medicare plan coverage options during the annual Open Enrollment Period that begins every year on October 15th and continues through December 7th.

Need a fast way to see how your Medicare Advantage or Medicare Part D plan is changing next year?

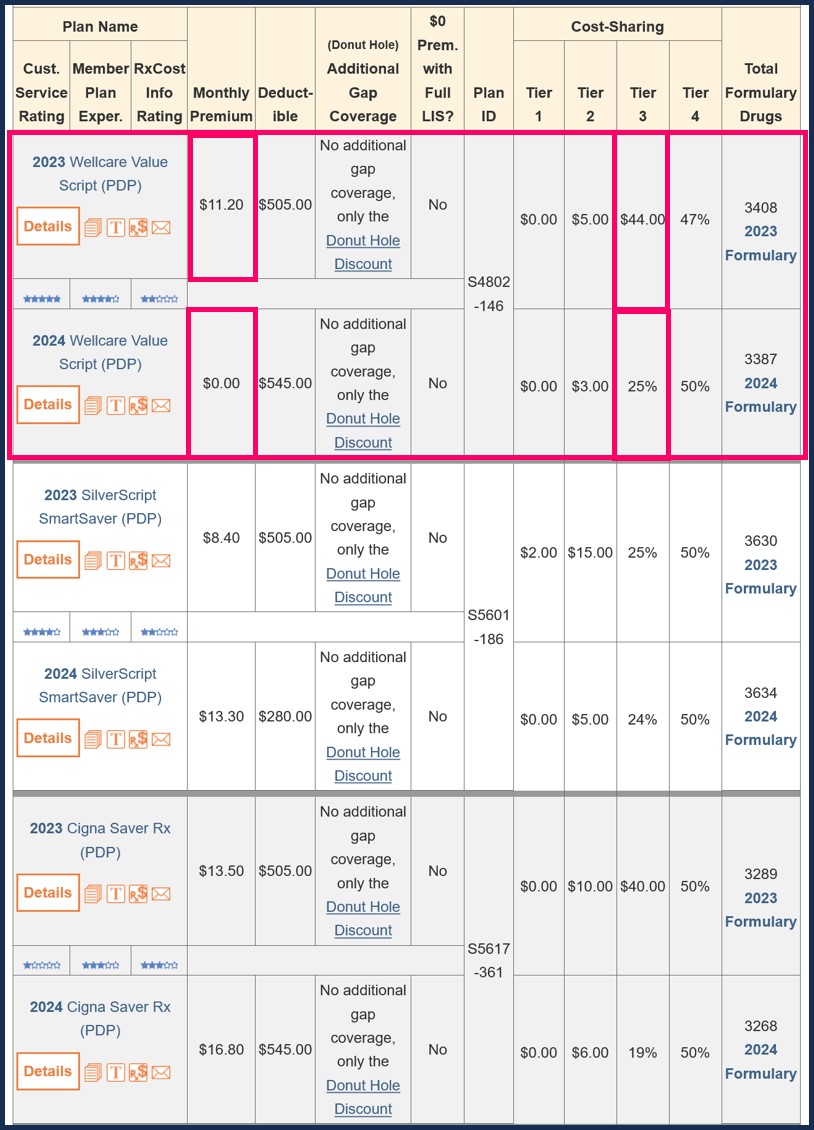

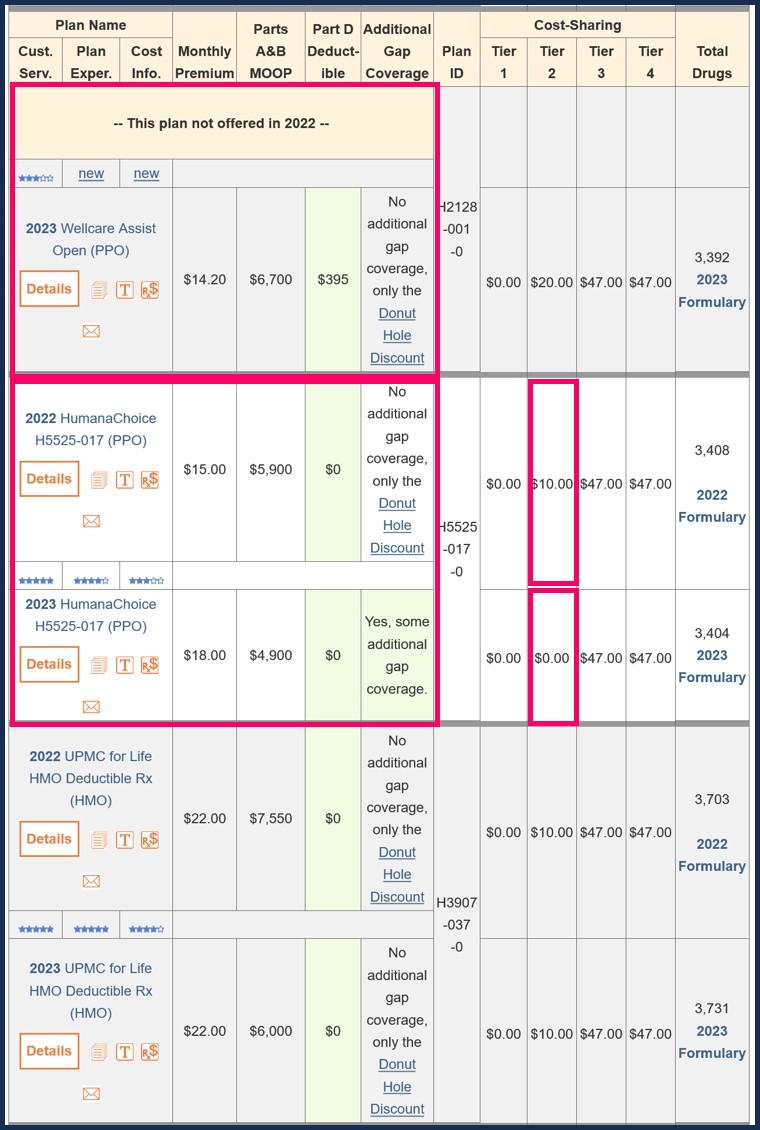

Our PDP-Compare.com and MA-Compare.com tools allow you to compare changes in all stand-alone Medicare Part D prescription drug plans (PDPs) or Medicare Advantage plans (MAs or MAPDs) across the country.

Our comparison tools show changes in monthly premiums and plan designs, as well as changes in copayments or coinsurance rates for different drug tiers.

Both the PDP-Compare and MA-Compare tools also show the Medicare Part D plans or Medicare Advantage plans that will be discontinued or added next year. The MA-Compare tool includes links to the health coverage details of all Medicare Advantage plans.

Example of PDP-Compare.com - Showing how stand-alone Medicare Part D plans can change year-to-year.

Example of MA-Compare.com - showing how Medicare Advantage plans can change year-to-year.

Browse FAQ Categories

Q1 Quick Links

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service