What is the Medicare Part D "Lesser Of" logic?

In the Medicare Part D prescription drug program, the "lesser of" logic ensures that Medicare beneficiaries are not paying more than their Medicare plan's negotiated retail price for their drugs - even when their plan's cost-sharing could amount to a higher price.

For example, if your local pharmacy offers an every-day retail pharmacy price of $4 for your prescription (not a sale price) and the retail price is less than your Medicare Part D plan's copay of $8, you will be charged the lower every-day retail price of $4. In the same way, if $4 is your Medicare Part D plan's negotiated retail price for your prescription, you can expect to pay the plan's $4 negotiated retail drug price and not your plan's $8 co-pay.

Why is the lessor of rule so important to you?

Question: Where can I find the "lessor of" rule stated?

You can find the "lesser of" logic in your own Medicare Part D drug plan's Evidence of Coverage document (the 200+ page book that you received either electronically or printed when you enrolled in your plan) and the rule should read something like:

For example, if your local pharmacy offers an every-day retail pharmacy price of $4 for your prescription (not a sale price) and the retail price is less than your Medicare Part D plan's copay of $8, you will be charged the lower every-day retail price of $4. In the same way, if $4 is your Medicare Part D plan's negotiated retail price for your prescription, you can expect to pay the plan's $4 negotiated retail drug price and not your plan's $8 co-pay.

Why is the lessor of rule so important to you?

When you choose a Medicare Part D plan, you may find that one of your low-costing medications is now on a high-costing drug tier - and this may cause some undue stress as you contemplate your increased drug costs. For example, you may use a common medication that has a retail price around $10, but your Medicare Part D plan has moved the low-cost drug to formulary Tier 3 that has a $30 co-pay. You will not pay the $30 co-pay, but instead, never pay more than your plans $10 negotiated retail drug price.

Examples of the lessor of logic

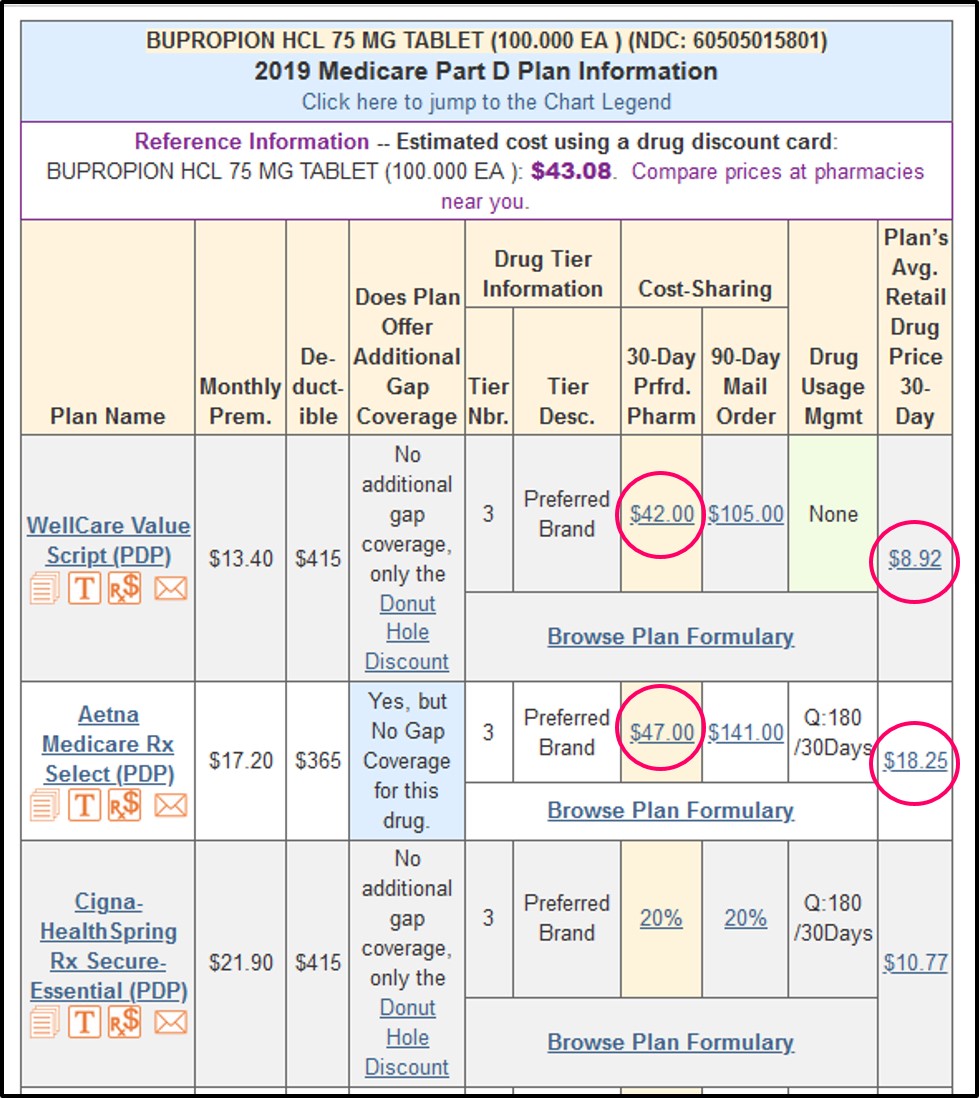

The following example is from the 2019 Q1Rx Drug Finder (Q1Rx.com) using a low-cost generic (Bupropion HCL) that is organized by many Medicare Part D plans as a Tier 3 Preferred Brand Drug. You can see that the first Medicare plan's average retail price for this drug is $8.92, but the co-pay is $42 - using the "lessor of logic", you would pay the $8.92 retail price and not the $42 co-pay. The second Medicare Part D plan in the list shows an average retail cost of $18.25 with a $47 co-pay, again, you would pay no higher than the retail cost of $18.25 and not the $47 co-pay. (See Q1Rx.com/2019/FL/60505015801)

Examples of the lessor of logic

The following example is from the 2019 Q1Rx Drug Finder (Q1Rx.com) using a low-cost generic (Bupropion HCL) that is organized by many Medicare Part D plans as a Tier 3 Preferred Brand Drug. You can see that the first Medicare plan's average retail price for this drug is $8.92, but the co-pay is $42 - using the "lessor of logic", you would pay the $8.92 retail price and not the $42 co-pay. The second Medicare Part D plan in the list shows an average retail cost of $18.25 with a $47 co-pay, again, you would pay no higher than the retail cost of $18.25 and not the $47 co-pay. (See Q1Rx.com/2019/FL/60505015801)

Question: Where can I find the "lessor of" rule stated?

You can find the "lesser of" logic in your own Medicare Part D drug plan's Evidence of Coverage document (the 200+ page book that you received either electronically or printed when you enrolled in your plan) and the rule should read something like:

"If your covered drug costs less than the copayment amount listed in the chart, you will pay that lower price for the drug. You pay either the full price of the drug or the copayment amount, whichever is lower." [emphasis added]

The "Lesser of Logic" applied in Medicare Part D prescription drug plans is also explained in the Centers for Medicare and Medicaid Services (CMS) Prescription Drug Benefit Manual, Chapter 5: Benefits and Beneficiary Protections, in Section 20.6 "Negotiated Prices".

In this section, CMS holds:

"Part D sponsors [such as Aetna or United HealthCare or WellCare] must provide enrollees with access to negotiated prices for covered Part D drugs as part of their qualified prescription drug coverage. This access to negotiated prices must be provided even when no benefits are otherwise payable on behalf of an enrollee due to the application of a deductible or other cost-sharing. Negotiated prices will take into account negotiated price concessions for covered Part D drugs that are passed through to enrollees at the point of sale, such as:(Rev. 14, Issued; 09-30-11, Effective: 09-30-11, Implementation: 09-30-11) [emphasis added]

• Discounts;

• Direct or indirect subsidies;

• Rebates; and

• Other direct or indirect remunerations

In addition, negotiated prices must include any applicable dispensing fees (discussed in section 20.7 [of the same CMS manual]).

Although negotiated prices do not have to be made available for drugs that are not covered Part D drugs, they must be made available throughout the benefit – including in any phase of the benefit, such as the deductible, in which an enrollee is responsible for 100 percent cost-sharing – for all covered Part D drugs. Part D sponsors must ensure that their payment systems are set up to charge beneficiaries the lesser of a drug’s negotiated price or applicable copayment amount in all phases of the benefit.

Example: A beneficiary’s drug is on a $10 cost-sharing tier. However, the negotiated price of the drug is $4. The beneficiary never pays more than $4.

In addition, uniform negotiated prices must be available to plan enrollees for a particular covered Part D drug when purchased from the same pharmacy. In other words, the negotiated price for a particular covered Part D drug purchased at a particular pharmacy must always be the same regardless of what phase of the Part D benefit an enrollee is in. (To the extent that the negotiated price fluctuates based on fluctuations in Average Wholesale Price (AWP), the actual cost to the beneficiary may vary from purchase to purchase; however, the negotiated rate, absent any contractual changes in the reimbursement rate between the pharmacy and the Part D sponsor, will remain constant for that drug.)"

This same "Lesser of Logic" concept was also repeated in other CMS examples:

Suppose your Medicare Part D plan has a $310 initial deductible (that is, you pay 100% of the first $310) and now you only have $75 remaining before you satisfy this Initial Deductible. You need a refill for one of your [Tier 3] medications and your drug purchase has a negotiated retail cost of $100. During your Initial Coverage phase, the co-payment for this Tier-3 medication is $40 (or you pay $40 and your Medicare Part D plan pays the remaining $60).

So in our example, you would pay the first $75 to leave the Initial Deductible phase and then have $25 that was left over [from the original $100 drug cost] in the Initial Coverage phase [this transaction is also known as a "Straddle Claim"]. Since the remaining $25 retail cost is less than the $40 co-pay, you would pay the $25 for a total of $100. You would not pay the $40 co-pay because your total would then be $115 - which is more than the $100 negotiated retail drug price.

Again, you would pay the "lesser of" either the retail price of $100 or the co-payment total of $115.

Browse FAQ Categories

Q1 Quick Links

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service