What is the 2019 standard Initial Coverage Limit and how does the ICL work?

The 2019 standard Initial Coverage Limit (ICL) is $3,820.

The Initial Coverage Limit is the measured by the retail cost of your drug purchases and is used to determine when you leave your Medicare plan's Initial Coverage Phase and enter the Donut Hole or Coverage Gap portion of your Medicare Part D prescription drug plan.

For example, if you purchase a medication with a retail cost of $100 and your Medicare Part D plan pays $70 toward the prescription and you pay a $30 co-payment, the total retail value of $100 counts toward meeting your Initial Coverage Limit and moves you $100 closer to entering the Donut Hole.

The standard Initial Coverage Limit (entry point to the Coverage Gap or Donut Hole) can vary each year.

In 2006, at the start of the Medicare Part D program, the Initial Coverage Limit was $2,250 and now the ICL has increased in 2019 to $3,820.

You can view how the standard Initial Coverage Limit has changed each year since 2006 here: https://q1medicare.com/PartD-The-MedicarePartDOutlookAllYears.php.

The Initial Coverage Limit can vary between Medicare Part D plan providers.

In other words, with some Medicare plans you will enter the Donut Hole or Coverage Gap faster than with other Medicare plans. Although currently, all stand-alone Medicare Part D plans are using the standard ICL ($3,820), some 2019 Medicare Advantage plans that include prescription drug coverage (MAPDs) have an Initial Coverage Limit ranging from $3,010 to $8,000. You can click here to read more about 2019 Medicare Advantage plans that have an increased or decreased Initial Coverage Limit.

Important Part #1:

The Initial Coverage Limit only includes purchases of formulary medications. Purchases of non-formulary drugs, over-the-counter (OTC) drugs, or bonus drugs (such as ED drugs like Viagra) do not count toward reaching your ICL.

Important Part #2:

The retail cost of your formulary medications counts toward your Initial Coverage Limit and the negotiated retail price of a medication can vary at different network pharmacies. For instance, the medication "Amlodipine Besylate/Benazepril Hydrochloride CAP 10-20MG" is covered by the 2019 Aetna Medicare Rx Select (PDP) at all network pharmacies. However, the retail costs for a 30-day supply at a CVS pharmacy is $2.27 (preferred pharmacy) and the retail cost for the same medication at a Walmart pharmacy is $19.50 (standard or non-preferred pharmacy) (source: Medicare.gov Plan Finder, 08.10.2019). So, if you filled your prescription for this medication at a CVS pharmacy, you would have around $17.23 less counted toward the 2019 ICL.

Important Part #3:

Please note that a single purchase of an expensive medication (for example, a medication with a retail cost of over $3,820), will exceed the Initial Coverage Limit and push you through the Initial Coverage Phase and into the Coverage Gap (this is called a straddle claim).

A Summary of your Medicare Part D plan coverage

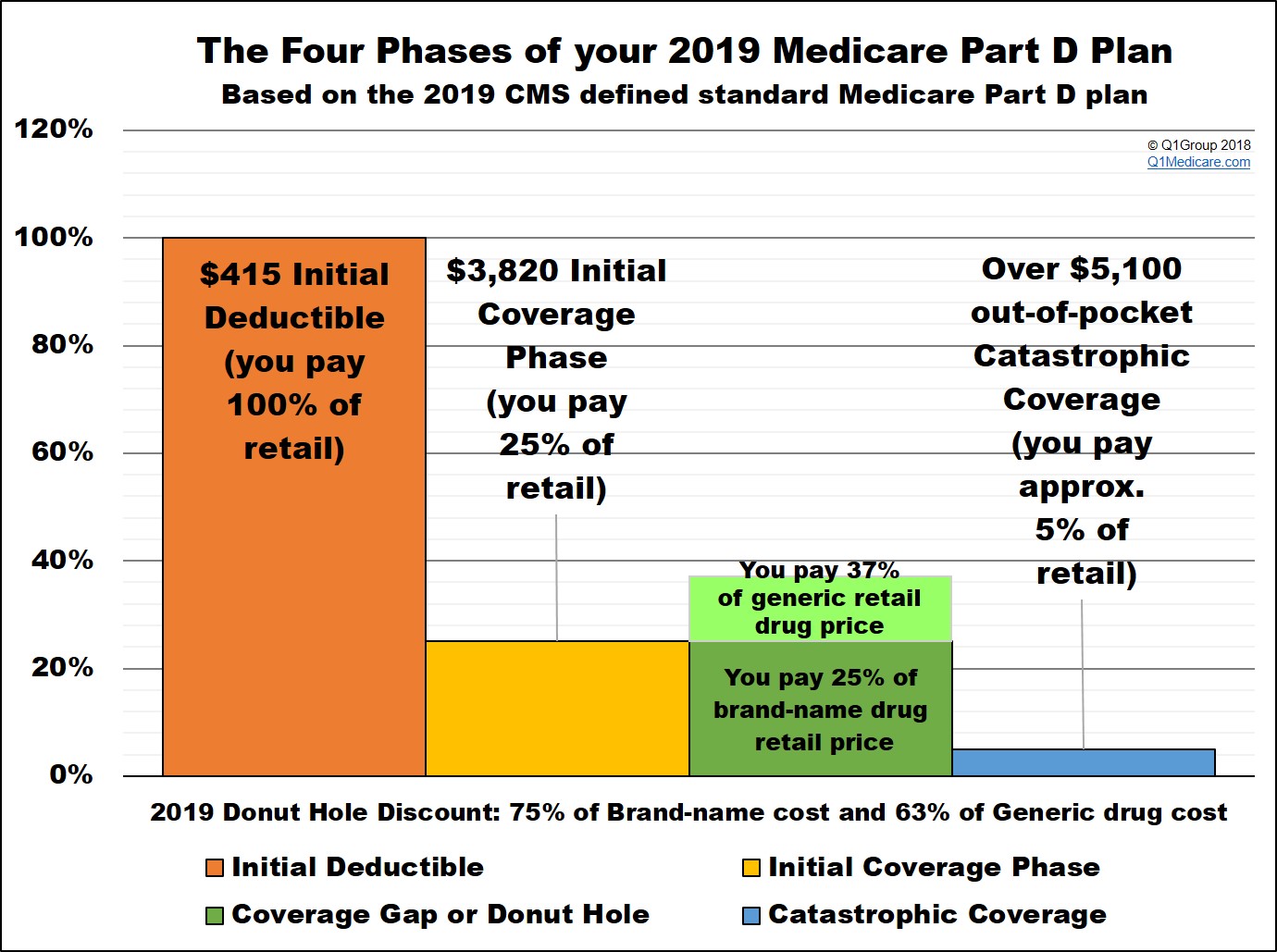

Again, the Initial Coverage Limit is the value that determines when you leave your Medicare Part D plan's Initial Coverage Phase and enter into the Donut Hole or Coverage Gap. So once you have received coverage for formulary drugs worth a retail value of over $3,820, you will enter the 2019 Donut Hole. As a reminder, your Medicare Part D prescription drug plan includes four different phases or parts:

(1) The Initial Deductible is where you pay 100% of your retail drug costs until you reach your deductible amount ($415 in 2019). Many people will enroll in a Medicare prescription drug plan with a $0 deductible and effectively skip-over this first phase. The Initial Deductible has no effect on when you enter the Donut Hole, but will affect when you exit the Donut Hole and enter the Catastrophic Coverage phase.

(2) The Initial Coverage Phase is where you and your Medicare Part D plan share in the cost of your medication purchases based on your plan's cost-sharing (such as a $30 co-payment or 25% co-insurance). When the retail value of your drug purchases exceeds your Initial Coverage Limit (ICL or Donut Hole entry point), you will leave your Initial Coverage Phase and enter the Coverage Gap or Donut Hole.

Please note that the Initial Coverage Limit is not measured by what you have spent on medications. Instead, the ICL is the total retail value of your prescription drug purchases. So this is the amount that you pay for your prescriptions plus what your Medicare Part D plan is paying.

So if you buy a $1,000 prescription drug and you pay a $60 co-pay (the Medicare Part D plan pays the other $940), the total $1,000 retail cost counts toward your 2019 Initial Coverage Limit of $3,820. In this case, after the $1,000 drug purchase, you have $2,820 remaining in drug purchases before entering the 2019 Donut Hole.

You may find that your plan's retail drug costs are not the same as another Medicare Part D plan's cost. In other words, you might buy a medication like Atorvastatin (10mg) and your plan will have a retail price of $20, although you may only pay a $4 co-pay. However, a friend in another Part D plan may use the same medication and also have a $4 co-pay, but their plan's retail price for Atorvastatin (10mg) is around $7. So, the same medication can have the same co-pay, but different negotiated retail prices depending on the Medicare plan - and so the different retail costs have different impacts on the Initial Coverage Limit.

As you can imagine, if you purchase an expensive medication (for example, with a retail cost of over $3,820), your coverage costs may be $750 or less, but the retail cost may exceed the Initial Coverage Limit and push you through the Initial Coverage Phase and into the Coverage Gap - with just one single purchase (this is called a straddle claim).

The standard Initial Coverage Limit (entry point to the Coverage Gap or Donut Hole) can vary each year. For instance, the Initial Coverage Limit is $3,820 in 2019 as compared to the Initial Coverage Limit of $2,250 in 2006. You can view the standard Initial Coverage Limits for the past several years here: https://q1medicare.com/2019

At times, the Initial Coverage Limit can also vary between Medicare Part D plan providers. With the approval of Medicare (CMS) Medicare Part D plans are allowed to deviate from the annual standard Initial Coverage Limit value. You can click here to read more about 2019 Medicare Advantage plans that have an increased or decreased Initial Coverage Limit.

(3) The Coverage Gap or Donut Hole is the plan phase you enter once you exceed the Initial Coverage Limit and where you were originally responsible for 100% of your drug costs (so this was like a second deductible phase). However, with the introduction of the donut hole discount in 2011, beneficiaries were no longer responsible for 100% of the cost of their purchases in the donut hole. You can read more about the current Donut Hole Discount here: https://Q1FAQ.com/470.html

In 2019 the donut hole discount will increase to a 75% discount on brand-name drugs and a 63% discount on generic drugs (you will pay 25% of your plan's negotiated retail cost for brand-name prescriptions and 37% of the retail cost for generics). The Donut Hole will be reduced to a fixed 25% co-insurance cost-sharing structure for all formulary drugs in 2020 and continue at the 25% cost-sharing rate thereafter - at that point, the Donut Hole is considered "closed".

(4) The Catastrophic Coverage Phase is the last phase of your Medicare Part D plan and you enter once your total out-of-pocket drug costs exceed a certain point (over $5,100 in 2019). During this phase you will exit the Donut Hole or Coverage Gap and will receive your medications at a low price, paying $8.50 or 5% of the retail price (which ever is higher) for the remainder of the year****.

* 25% co-pay

** 75% Discount

*** 63% Discount

**** the higher of 5% of retail or $3.40 for generic drugs and the higher of 5% of retail $8.50 for all other formulary drugs (80% paid by Medicare, 15% paid by Medicare plan, and around 5% by plan member)

The Initial Coverage Limit is the measured by the retail cost of your drug purchases and is used to determine when you leave your Medicare plan's Initial Coverage Phase and enter the Donut Hole or Coverage Gap portion of your Medicare Part D prescription drug plan.

For example, if you purchase a medication with a retail cost of $100 and your Medicare Part D plan pays $70 toward the prescription and you pay a $30 co-payment, the total retail value of $100 counts toward meeting your Initial Coverage Limit and moves you $100 closer to entering the Donut Hole.

The standard Initial Coverage Limit (entry point to the Coverage Gap or Donut Hole) can vary each year.

In 2006, at the start of the Medicare Part D program, the Initial Coverage Limit was $2,250 and now the ICL has increased in 2019 to $3,820.

You can view how the standard Initial Coverage Limit has changed each year since 2006 here: https://q1medicare.com/PartD-The-MedicarePartDOutlookAllYears.php.

The Initial Coverage Limit can vary between Medicare Part D plan providers.

In other words, with some Medicare plans you will enter the Donut Hole or Coverage Gap faster than with other Medicare plans. Although currently, all stand-alone Medicare Part D plans are using the standard ICL ($3,820), some 2019 Medicare Advantage plans that include prescription drug coverage (MAPDs) have an Initial Coverage Limit ranging from $3,010 to $8,000. You can click here to read more about 2019 Medicare Advantage plans that have an increased or decreased Initial Coverage Limit.

Important Part #1:

The Initial Coverage Limit only includes purchases of formulary medications. Purchases of non-formulary drugs, over-the-counter (OTC) drugs, or bonus drugs (such as ED drugs like Viagra) do not count toward reaching your ICL.

Important Part #2:

The retail cost of your formulary medications counts toward your Initial Coverage Limit and the negotiated retail price of a medication can vary at different network pharmacies. For instance, the medication "Amlodipine Besylate/Benazepril Hydrochloride CAP 10-20MG" is covered by the 2019 Aetna Medicare Rx Select (PDP) at all network pharmacies. However, the retail costs for a 30-day supply at a CVS pharmacy is $2.27 (preferred pharmacy) and the retail cost for the same medication at a Walmart pharmacy is $19.50 (standard or non-preferred pharmacy) (source: Medicare.gov Plan Finder, 08.10.2019). So, if you filled your prescription for this medication at a CVS pharmacy, you would have around $17.23 less counted toward the 2019 ICL.

Important Part #3:

Please note that a single purchase of an expensive medication (for example, a medication with a retail cost of over $3,820), will exceed the Initial Coverage Limit and push you through the Initial Coverage Phase and into the Coverage Gap (this is called a straddle claim).

A Summary of your Medicare Part D plan coverage

Again, the Initial Coverage Limit is the value that determines when you leave your Medicare Part D plan's Initial Coverage Phase and enter into the Donut Hole or Coverage Gap. So once you have received coverage for formulary drugs worth a retail value of over $3,820, you will enter the 2019 Donut Hole. As a reminder, your Medicare Part D prescription drug plan includes four different phases or parts:

(1) The Initial Deductible is where you pay 100% of your retail drug costs until you reach your deductible amount ($415 in 2019). Many people will enroll in a Medicare prescription drug plan with a $0 deductible and effectively skip-over this first phase. The Initial Deductible has no effect on when you enter the Donut Hole, but will affect when you exit the Donut Hole and enter the Catastrophic Coverage phase.

(2) The Initial Coverage Phase is where you and your Medicare Part D plan share in the cost of your medication purchases based on your plan's cost-sharing (such as a $30 co-payment or 25% co-insurance). When the retail value of your drug purchases exceeds your Initial Coverage Limit (ICL or Donut Hole entry point), you will leave your Initial Coverage Phase and enter the Coverage Gap or Donut Hole.

Please note that the Initial Coverage Limit is not measured by what you have spent on medications. Instead, the ICL is the total retail value of your prescription drug purchases. So this is the amount that you pay for your prescriptions plus what your Medicare Part D plan is paying.

So if you buy a $1,000 prescription drug and you pay a $60 co-pay (the Medicare Part D plan pays the other $940), the total $1,000 retail cost counts toward your 2019 Initial Coverage Limit of $3,820. In this case, after the $1,000 drug purchase, you have $2,820 remaining in drug purchases before entering the 2019 Donut Hole.

You may find that your plan's retail drug costs are not the same as another Medicare Part D plan's cost. In other words, you might buy a medication like Atorvastatin (10mg) and your plan will have a retail price of $20, although you may only pay a $4 co-pay. However, a friend in another Part D plan may use the same medication and also have a $4 co-pay, but their plan's retail price for Atorvastatin (10mg) is around $7. So, the same medication can have the same co-pay, but different negotiated retail prices depending on the Medicare plan - and so the different retail costs have different impacts on the Initial Coverage Limit.

As you can imagine, if you purchase an expensive medication (for example, with a retail cost of over $3,820), your coverage costs may be $750 or less, but the retail cost may exceed the Initial Coverage Limit and push you through the Initial Coverage Phase and into the Coverage Gap - with just one single purchase (this is called a straddle claim).

The standard Initial Coverage Limit (entry point to the Coverage Gap or Donut Hole) can vary each year. For instance, the Initial Coverage Limit is $3,820 in 2019 as compared to the Initial Coverage Limit of $2,250 in 2006. You can view the standard Initial Coverage Limits for the past several years here: https://q1medicare.com/2019

At times, the Initial Coverage Limit can also vary between Medicare Part D plan providers. With the approval of Medicare (CMS) Medicare Part D plans are allowed to deviate from the annual standard Initial Coverage Limit value. You can click here to read more about 2019 Medicare Advantage plans that have an increased or decreased Initial Coverage Limit.

(3) The Coverage Gap or Donut Hole is the plan phase you enter once you exceed the Initial Coverage Limit and where you were originally responsible for 100% of your drug costs (so this was like a second deductible phase). However, with the introduction of the donut hole discount in 2011, beneficiaries were no longer responsible for 100% of the cost of their purchases in the donut hole. You can read more about the current Donut Hole Discount here: https://Q1FAQ.com/470.html

In 2019 the donut hole discount will increase to a 75% discount on brand-name drugs and a 63% discount on generic drugs (you will pay 25% of your plan's negotiated retail cost for brand-name prescriptions and 37% of the retail cost for generics). The Donut Hole will be reduced to a fixed 25% co-insurance cost-sharing structure for all formulary drugs in 2020 and continue at the 25% cost-sharing rate thereafter - at that point, the Donut Hole is considered "closed".

(4) The Catastrophic Coverage Phase is the last phase of your Medicare Part D plan and you enter once your total out-of-pocket drug costs exceed a certain point (over $5,100 in 2019). During this phase you will exit the Donut Hole or Coverage Gap and will receive your medications at a low price, paying $8.50 or 5% of the retail price (which ever is higher) for the remainder of the year****.

|

When you purchase a formulary medication

with a $100 retail cost in 2019

|

||||||

| Retail Cost (ICL) | You Pay | Medicare Plan Pays | Pharma Mfgr Pays | Gov. pays | Amount toward your TrOOP | |

| Initial Deductible | $100 | $100 | $0 | $0 | $0 | $100 |

| Initial Coverage Phase * | $100 | $25 | $75 | $0 | $0 | $25 |

| Coverage Gap - brand-name ** | $100 | $25 | $5 | $70 | $0 | $95 |

| Coverage Gap - generic *** | $100 | $37 | $63 | $0 | $0 | $37 |

| Catastrophic Coverage (generic)**** | $100 | $5 | $15 | $0 | $80 | $5 |

* 25% co-pay

** 75% Discount

*** 63% Discount

**** the higher of 5% of retail or $3.40 for generic drugs and the higher of 5% of retail $8.50 for all other formulary drugs (80% paid by Medicare, 15% paid by Medicare plan, and around 5% by plan member)

News Categories

Pets are Family Too!

Use your drug discount card to save on medications for the entire family ‐ including your pets.

- No enrollment fee and no limits on usage

- Everyone in your household can use the same card, including your pets

Your drug discount card is available to you at no cost.

Q1 Quick Links

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service