On January 15, 2021, the Centers for Medicare and

Medicaid Services (CMS) released

the "Announcement of Calendar Year (CY) 2022 Medicare Advantage (MA) Capitation Rates and Part C and Part D Payment Policies" (Announcement) that included finalized defined

standard benefits for 2022 Medicare Part D prescription drug plan coverage and other changes to the Medicare program.

Why is the Medicare Part D Defined Standard Benefit important?

Each year, CMS releases the Medicare Part D benefit parameters for the "Defined Standard Benefit" and Medicare Part D plans use this information to determine minimum Part D drug plan coverage for the up-coming plan year. You can use the CMS parameters as a preview of how your Medicare

Part D prescription drug plan coverage may change in January, 2022 (for example, if you currently pay a $445 deductible, your deductible in 2022 may be $480).

Actual plan options and benefit details will be available for your review beginning October

1, 2021 and you can make 2022 plan changes during the fall annual Open Enrollment Period (AEP) (October 15th through December 7th).

How will these changes in 2022 Medicare Part D plan coverage affect you?

If you are trying to get an idea of your 2022 prescription drug spending budget, you can use our 2022 Donut Hole calculator (found at PDP-Planner.com/2022) to estimate your actual out-of-pocket spending based on your estimated mix of generic and brand-name drugs purchased in the 2022 Coverage Gap.

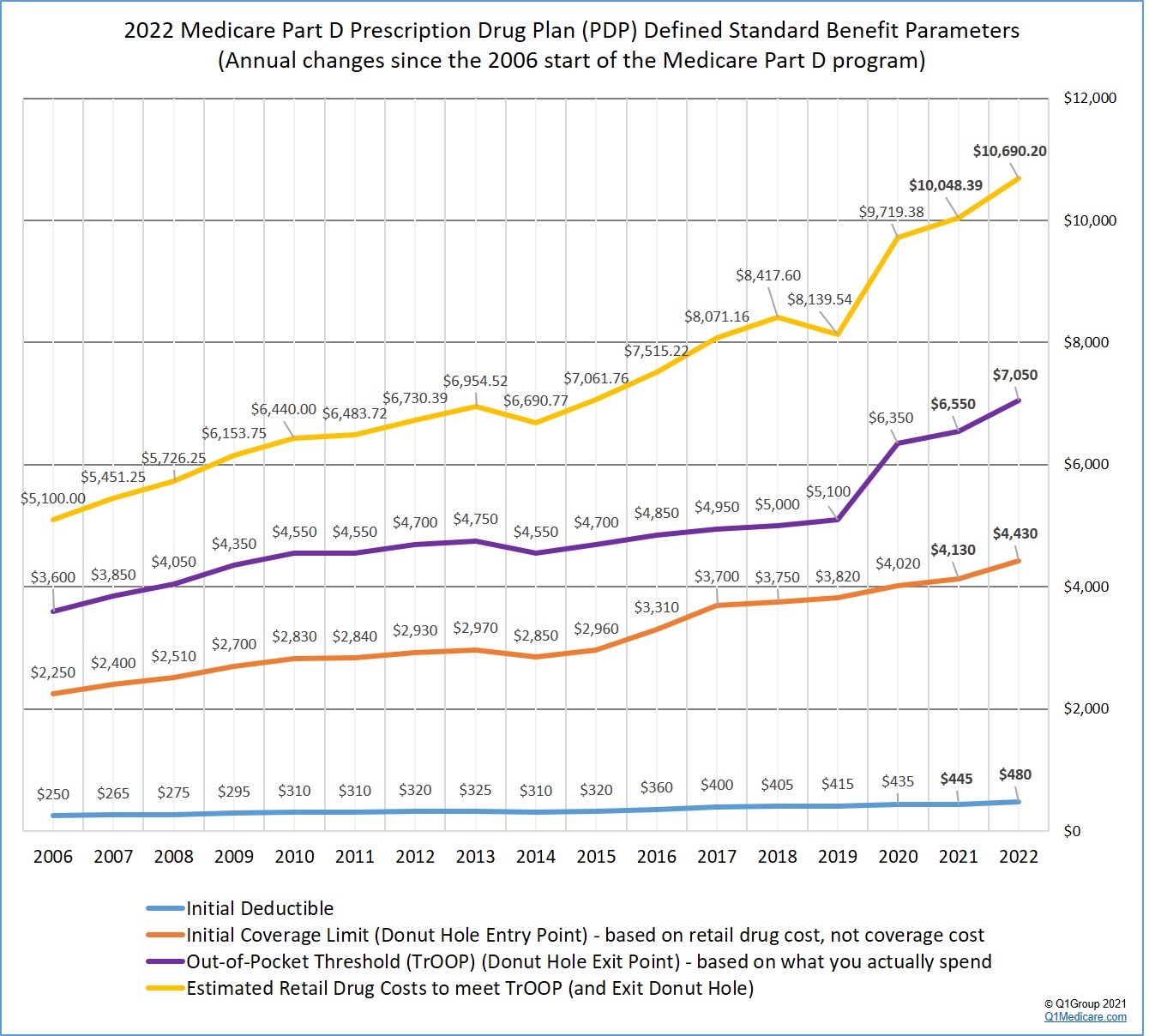

As an overview, the following graph shows the 2022 Medicare Part D plan parameters and how standard Medicare Part D plan coverage has changed since the 2006 beginning of the Medicare Part D program.

Based on the 2022 Announcement, here are the changes to the standard Medicare Part D prescription drug coverage:

- The standard 2022 Initial Deductible will increase almost 8%.

The 2022 standard Initial Deductible will increase $35 to $480 from the current 2021 standard Initial Deductible of $445. As reference, the 2020 standard Initial Deductible was $435.

What this means to you: The Initial Deductible is the amount that you must pay before your Medicare Part D plan begins to share in the cost of coverage. If you enroll in a Medicare Part D prescription drug plan with a standard Initial Deductible, you will spend slightly more out-of-pocket in 2022 before your plan coverage begins.

As a note, the majority of 2021 Medicare Part D plans have an initial deductible - and we expect this trend to continue in 2022.

But, as we see in 2021, many popular Medicare Part D plans also exclude lower-costing Tier 1 and Tier 2 drugs from the deductible, providing plan Members with immediate coverage for some lower-costing medications.

The Initial Deductible and the Donut Hole: The Initial Deductible will not affect when you enter the Donut Hole or Coverage Gap, but will impact when you leave the Donut Hole and enter the Catastrophic Coverage portion of your Medicare Part D plan coverage. In other words, what you spend toward your Initial Deductible is counted toward your total out-of-pocket spending threshold or TrOOP (see below for more about TrOOP).

- The

Initial Coverage Limit will increase around 7%.

The 2022 Initial Coverage Limit (ICL) will increase $300 to $4,430 from the current 2021 ICL of $4,130 (as reference, the 2020 ICL was $4,020). The Initial Coverage Limit marks the point where you enter the Donut Hole or Coverage Gap. Medicare Part D beneficiaries enter the Donut Hole when the total negotiated retail value of their prescription drug purchases exceeds their plan’s Initial Coverage Limit.

What this means to you: You will be able to buy slightly more medications before reaching the 2022 Donut Hole or Coverage Gap (assuming that the retail price of your medications does not increase over time).

- Will you enter the 2022 Donut Hole?

If you purchase medications with an average retail value of over $370 per month (based on your current retail drug prices remaining stable), then you will enter the 2022 Donut Hole at some point during the year. For more information, please see our 2022 Donut Hole calculator to estimate when (or if) you will enter the Donut Hole: https://PDP-Planner.com/2022

- The 2022 Donut Hole discount for generic drugs remains at 75%.

If you reach the 2022 Donut Hole or Coverage Gap phase of your Medicare Part D plan coverage, the drug discount is 75%. So your generic formulary drug costs in the Donut Hole will be 25% of your plan's negotiated retail prices.

What this means to you: If you are in the 2022 Donut Hole and your generic medication has a retail cost of $100, you will pay only $25 for a refill. And the $25 that you spend for a formulary drug will count toward your 2022 out-of-pocket spending limit or TrOOP of $7,050.

- The

Donut Hole discount for brand-name drugs remains at 75%.

The 2022 brand-name drug Donut Hole discount also remains at 75% (you pay 25% of retail costs). The pharmaceutical industry will be responsible for 70% of the cost of medications in the Coverage Gap, therefore you will receive credit for 95% of the retail drug cost toward meeting your 2022 total out-of-pocket maximum or Donut Hole exit point (the 25% of retail costs you pay plus the 70% drug manufacturer discount).

What this means to you: If you reach the 2022 Donut Hole and purchase a brand-name medication with a retail cost of $100, you will pay $25 for the formulary medication, and receive $95 credit toward meeting your 2022 out-of-pocket spending limit – or Donut Hole exit point.

- The amount you need to spend (TrOOP) to exit the 2022 Donut Hole will increase almost 8%

Your 2022 Total Out-of-Pocket Cost (TrOOP) threshold will increase by $500 to $7,050 from the current 2021 TrOOP limit of $6,550. TrOOP is the actual dollar figure you must spend (or someone else spends on your behalf) to get out of the Donut Hole or Coverage Gap and into the Catastrophic Coverage phase of your Medicare Part D plan and TrOOP does not include monthly premiums or non-formulary purchases. As reference, the 2020 TrOOP limit was $6,350 and the 2019 TrOOP limit was $5,100.

What this means to you: If you reach the 2022 Donut Hole, you will need to spend slightly more money before exiting the Donut Hole and entering the 2022 Catastrophic Coverage portion of your Medicare Part D plan coverage.

The good news: As noted above, brand-name medication purchases in the 2022 Donut Hole are discounted by 75% (you pay 25%), but you will receive credit of 95% of the retail drug price toward meeting the 2022 TrOOP threshold.

Examples of your prescription purchases needed to meet TrOOP and exit the 2022 Donut Hole:

Example #1: Exiting the Donut Hole with your formulary drug mix is 91.76% brands and 8.24% generics

Using Medicare's past drug usage estimate*, the average person will have purchases of 91.76% brand drugs and 8.24% generic drugs while in the 2022 Donut Hole. So assuming your 2022 Part D plan has a $480 deductible and the retail cost of your drugs is about $891 per month, you can estimate your actual annual out-of-pocket drug costs to be around $3,032 before meeting the $7,050 TrOOP and exiting the 2022 Donut Hole - your Medicare Part D plan would spend about $3,637 and the pharmaceutical manufacturers would spend about $4,019. (As a note, last year, CMS estimated that people in the 2021 Donut Hole would purchase 89.50% brand drugs and 10.50% generic drugs.)

The total retail value of your drug purchases needed to exit the Donut Hole would be around $10,690 (not adjusting for dispensing and vaccine fees). We are also not including your monthly premium costs in this estimate.

Example #2: Exiting the Donut Hole when your formulary drug mix is 100% generics

If you purchase only generic drugs (100% generic) in the Donut Hole - and again, we assume your Part D has a $480 deductible and the retail cost of your drugs is about $2,230 per month, you can expect your estimated annual costs to be $7,050 (or the same as the 2022 TrOOP) before exiting the Donut Hole - your Medicare Part D plan would spend about $19,710 and the pharmaceutical manufacturers would spend $0.

The total retail value of your drug purchases needed to exit the Donut Hole would be $26,760.

Example #3: Exiting the Donut Hole when your Donut Hole drug mix is 100% brand-name

If you purchase only brand drugs (100% brands) - and assuming your Part D plan has a $480 deductible and the retail cost of your drugs is about $859 per month, you can expect your actual annual costs to be around $2,936 before meeting the $7,050 TrOOP and exiting the Donut Hole - your Medicare Part D plan would spend about $3,256 and the pharmaceutical manufacturers would spend about $4,113.

The total retail value of your drug purchases needed to exit the Donut Hole would be $10,310.

What do these examples means to you?

You will spend more out-of-pocket to exit the 2022 Donut Hole as compared to 2021. In fact, the estimated retail value of drug purchases needed to exit the 2022 Donut Hole will increase over 6%. And you would exit the Donut Hole and enter Catastrophic Coverage faster by using brand-name medications in the Donut Hole since the pharmaceutical industry brand-name discount will accelerate you toward meeting your TrOOP.

* CMS estimates that a person will use a mix of 91.76% brand drugs and 8.24% generic drugs while in the 2022 Donut Hole (an increase in estimated brand-name drug use as compared to the 2021 estimated Donut Hole mix of 89.50% brand drugs and 10.50% generic drugs). As reference, in 2019, CMS estimated a mix of 89.31% brand drugs and 10.69% generic drugs and the estimated retail cost to meet 2019 TrOOP and exit the 2019 Donut Hole is $8,139.54; in 2018, the CMS retail drug-cost estimate was calculated using a mix of 87.9% brand drugs and 12.1% generic drugs and the estimated retail cost to meet 2018 TrOOP and exit the 2018 Donut Hole is $8,417.60.

Our Donut Hole calculations vs. the CMS cost estimate:

Please note, as shown in the examples above, our estimated cost using our Donut Hole Calculator is $10,690 which is a slightly different than the CMS total retail drug cost estimate. The variation between our calculations and CMS is because of rounding differences and the consideration of small "dispensing" and "vaccine administration fees" that are being used in the CMS calculation.

Still not sure how the 2022 Donut Hole or Coverage Gap functions?

As noted above, to help you visualize how your current drug spending relates to your Medicare Part D plan coverage, we have our updated 2022 Donut Hole calculator online at: PDP-Planner.com/2022. Our Donut Hole calculator helps you estimate what you can expect to pay throughout the different phases of your 2022 Medicare Part D plan coverage. We have several options for you to choose the percentage of generic and brand drugs you use and you can even change your mix of prescriptions to be 100% generic or 100% brand.

To get you started, you can click here to see an example of the 2022 Medicare prescription drug plan phases for someone with $800 per month brand drug retail cost and has the standard $480 deductible.

(Spoiler alert: If the retail cost of your formulary medications is $800 per month, you can expect to spend about $2,760 out-of-pocket in 2022 - assuming a $480 deductible and an average brand-name cost-sharing of 25% of retail - and not including monthly premiums).

- Will you exit the Donut Hole and enter the 2022 Catastrophic Coverage phase?

Based on CMS drug purchase estimates, if your monthly retail formulary drug costs are over $370, you will enter the 2022 Donut Hole and if your retail drug costs are over $891 per month, you will exit the 2022 Donut Hole and enter Catastrophic Coverage portion of your Medicare Part D plan.

- 2022 fixed Catastrophic Coverage

costs increase slightly.

The Catastrophic Coverage portion of your Medicare Part D plan begins when you leave the Coverage Gap or Donut Hole. In the 2022 Catastrophic Coverage phase, you pay a minimum of $9.85 for brand drugs or $3.95 for generics (or 5% of retail costs, whichever is higher). As reference, in 2021 Catastrophic Coverage phase, you pay a minimum of $9.20 for brand drugs or $3.70 for generics (or 5%, whichever is higher).

What this means to you: If you purchase a brand name medication with a retail price of over $197 or a generic medication with a retail price of over $79, you will pay 5% of retail or more than the minimum $9.85 for brand drugs or $3.95 for generics.

For example, if you are using the expensive medication IMBRUVICA 140 MG CAPSULE (90 EA) (NDC: 57962014009), your monthly retail drug costs may be over $4,500, so your catastrophic coverage cost would be approximately $225 per month since this 5% of retail cost is more than the minimum $9.85 brand-name catastrophic coverage cost (based on 2020 retail drug costs).

Additional 2022 and 2023 Information provided by the Centers for Medicare and Medicaid Services

- On June 2, 2020, CMS published the final rule for "Medicare and Medicaid Programs; Contract Year 2021 and 2022 Policy and Technical Changes to the Medicare Advantage Program, Medicare Prescription Drug Benefit Program, Medicaid Program, Medicare Cost Plan Program, and Programs of All-Inclusive Care for the Elderly" - that "was primarily intended to implement certain changes before the contract year 2021, stemming from the Bipartisan Budget Act of 2018 (BBA of 2018) and the 21st Century Cures Act (Cures Act). That final rule also codified several existing CMS policies and implemented other technical changes." For example, in the final regulations, CMS codified Special Enrollment Periods (SEPs) dealing with exception conditions or circumstances such as government-declared major disasters.

- In a related final rule released in January 2021, CMS added several other future enhancements to the Medicare Part D and Medicare Advantage plan program:

-- All 2023 Medicare plans will provide "Beneficiary Real Time Benefit Tool (RTBT)"

Starting on January 1, 2023, CMS will require all Medicare prescription drug plans to provide an online tool (Beneficiary Real Time Benefit Tool (RTBT)) so that plan members could instantly see formulary details and shop for the best-priced formulary medications or find low-cost alternative medications. (see § 423.128)

According to CMS, Medicare drug plan enrollees will "have access to real-time formulary and benefit information, including cost-sharing, to shop for lower-cost alternative therapies under their prescription drug benefit plan. [Plan members] would be able to compare cost sharing to find the most cost-effective prescription drugs for their health needs. For example, if a doctor recommends a specific cholesterol-lowering drug, the enrollee could look up what the copay would be and see if a different, similarly effective option might save the enrollee money. With this tool, enrollees will be better able to know what they’ll need to pay before they’re standing at the pharmacy cash counter."

-- 2022 Medicare plans could add a second, lower-costing Specialty Drug Tier (Tier for preferred Specialty Drugs)

Since Medicare Part D plans currently have a Specialty Drug Tier with a fixed percentage cost-sharing structure (25% to 50% of retail), many of the higher-costing formulary drugs are still very expensive for plan members. Starting January 1, 2022, CMS will allow "Part D plans to have a second, “preferred” specialty tier with a lower cost sharing amount than their other specialty tier. This change is designed to give Part D plans more tools to negotiate better deals with manufacturers and lower out-of-pocket costs for enrollees in exchange for placing those products on the “preferred” specialty tier." (§§ 423.104, 423.560, and 423.578)

CMS also clarified that tiering exceptions within the specialty tier would be allowed: "[W]e did not propose to revise and are not revising § 423.578(c)(3)(ii), which requires Part D sponsors to provide coverage for a drug for which a tiering exception was approved at the cost sharing that applies to the preferred alternative. Because the exemption from tiering exceptions for specialty tier drugs under § 423.578(a)(6)(iii) as proposed would apply only to tiering exceptions to non-specialty tiers, the existing requirement at § 423.578(c)(3)(ii) will require Part D sponsors to permit tiering exception requests for drugs on the higher cost-sharing specialty tier to the lower cost-sharing, specialty tier."

-- 2022 Medicare drug plan will be required to submit Pharmacy Performance Measures to CMS

Medicare plans currently use internal measures to evaluate the performance of network pharmacies and starting on January 1, 2022, CMS will require "Part D plans to disclose pharmacy performance measures to CMS, which will enable CMS to better understand how such measures are applied. CMS will also be able to report pharmacy performance measures publicly to increase transparency on the process and to inform the industry in its new efforts to develop a standard set of pharmacy performance measures."

-- 2022 Medicare drug plans will continue implementing SUPPORT Act provisions combating the opioid epidemic

In the final rule, CMS also adds several additional provisions of the Substance Use-Disorder Prevention that Promotes Opioid Recovery and Treatment (SUPPORT) for Patients and Communities Act "that require Part D plans to educate beneficiaries on opioid risks, alternate pain treatments, and safe disposal of prescription drugs that are controlled substances, including opioids. The final rule also expands drug management programs, through which Part D plans review with providers opioid utilization trends that may put beneficiaries at-risk, and medication therapy management programs, through which Part D plans provide beneficiary-centric interventions." In addition, the final rule will implement "new requirements for Medicare Part D plan sponsors to report certain payment suspensions taken based on credible allegations of fraud against pharmacies when they are based on the SUPPORT Act authority (rather than previously existing bases such as contracts). It also implements new requirements that MA and Part D plan sponsors (including MA organizations offering MA-PD plans) report certain information related to inappropriate prescribing of opioids and any plan corrective actions to CMS via a secure internet portal."

https://www.cms.gov/newsroom/press-releases/ changes-medicare-advantage-and-part-d-will-provide-better-coverage- more-access-and-improved

https://www.cms.gov/newsroom/fact-sheets/contract-year-2022- medicare-advantage-and-part-d-final-rule-cms-4190-f2-fact-sheet

https://www.federalregister.gov/public-inspection/ 2021-00538/medicare-and-medicaid-programs-contract-year- 2022-policy-and-technical-changes-to-the-medicare

https://www.cms.gov/files/document/2022-announcement.pdf

https://www.cms.gov/newsroom/fact-sheets/2022-medicare-advantage-and-part-d-rate-announcement-fact-sheet

https://www.federalregister.gov/documents/2020/09/02/2020-19150/ medicare-and-medicaid-programs-clinical -laboratory-improvement-amendments-clia-and-patient

https://www.govinfo.gov/content/pkg/FR-2020-06-02/pdf/2020-11342.pdf

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service