When will I enter the Donut Hole?

You will enter into your Medicare Part D plan's Donut Hole or Coverage Gap when the total retail cost of your prescription purchases exceeds your Medicare Part D plan's Initial Coverage Limit (ICL) - and your ICL will change every year.

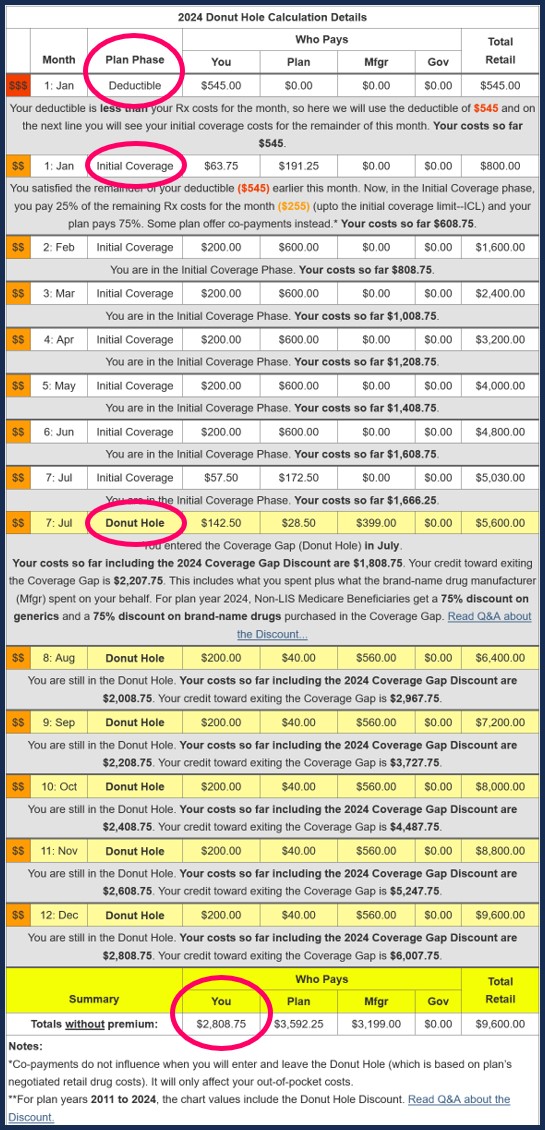

For example, in 2024, the standard Initial Coverage Limit is $5,030. So, in 2024, if you purchase formulary medications with a negotiated retail cost of over $420 per month, you will enter the Donut Hole sometime during 2024.

Question: But isn't the Donut Hole closed?

Not exactly. Although we say that the Donut Hole "closed" in 2020 since you receive a 75% discount on all formulary drugs, you will still leave your Medicare Part D plan's Initial Coverage Phase once your retail drug costs exceed the Initial Coverage Limit. And when you leave your Initial Coverage Phase, you will enter the Coverage Gap (Donut Hole) where the cost of your formulary medications can increase, decrease, or stay the same - depending on your Medicare drug plan, your cost-sharing, and the drug's retail price. You can click on our FAQ "Did the Coverage Gap or Donut Hole just close up and go away?" to read more.

Important Fact: 2024 is the last year that the Donut Hole will exist.

In 2025 one of the provisions of the Inflation Reduction Act (IRA) of 2022 is the elimination of the Coverage Gap (Donut Hole). Medicare Part D beneficiaries will stay in the Initial Coverage phase until they reach the maximum cap on out-of-pocket spending for Part D formulary drugs - RxMOOP - which is set at $2,000 for 2025. After reaching RxMOOP Medicare Part D beneficiaries will have a $0 copay for all formulary drugs.

Question: What if I use a brand-name formulary drug that costs $1,800 a month?

You will enter the Donut Hole during your third month of coverage. If you purchase a brand-name formulary medication with a negotiated retail cost of $1,800 per month, you will reach your Donut Hole in the third month of your Part D coverage or during your third purchase.

Your third purchase will be calculated as a straddle claim since the cumulative retail cost would now be $5,400 ($1,800 x 3), exceeding your $5,030 Initial Coverage Limit. This purchase would fall in both the Initial Coverage and Donut Hole phases. You would pay your cost-sharing applied in the Initial Coverage phase and the remaining amount $370 ($5,400 - $5,030 = $370) would fall into the Donut Hole where you would get a 75% discount -- you pay $92.50 (25% of $370). The Donut Hole cost-sharing ($92.50) plus the Initial Coverage cost-sharing are added together for this one purchase.

For example, in 2024, the standard Initial Coverage Limit is $5,030. So, in 2024, if you purchase formulary medications with a negotiated retail cost of over $420 per month, you will enter the Donut Hole sometime during 2024.

Question: But isn't the Donut Hole closed?

Not exactly. Although we say that the Donut Hole "closed" in 2020 since you receive a 75% discount on all formulary drugs, you will still leave your Medicare Part D plan's Initial Coverage Phase once your retail drug costs exceed the Initial Coverage Limit. And when you leave your Initial Coverage Phase, you will enter the Coverage Gap (Donut Hole) where the cost of your formulary medications can increase, decrease, or stay the same - depending on your Medicare drug plan, your cost-sharing, and the drug's retail price. You can click on our FAQ "Did the Coverage Gap or Donut Hole just close up and go away?" to read more.

Important Fact: 2024 is the last year that the Donut Hole will exist.

In 2025 one of the provisions of the Inflation Reduction Act (IRA) of 2022 is the elimination of the Coverage Gap (Donut Hole). Medicare Part D beneficiaries will stay in the Initial Coverage phase until they reach the maximum cap on out-of-pocket spending for Part D formulary drugs - RxMOOP - which is set at $2,000 for 2025. After reaching RxMOOP Medicare Part D beneficiaries will have a $0 copay for all formulary drugs.

Question: What if I use a brand-name formulary drug that costs $1,800 a month?

You will enter the Donut Hole during your third month of coverage. If you purchase a brand-name formulary medication with a negotiated retail cost of $1,800 per month, you will reach your Donut Hole in the third month of your Part D coverage or during your third purchase.

Your third purchase will be calculated as a straddle claim since the cumulative retail cost would now be $5,400 ($1,800 x 3), exceeding your $5,030 Initial Coverage Limit. This purchase would fall in both the Initial Coverage and Donut Hole phases. You would pay your cost-sharing applied in the Initial Coverage phase and the remaining amount $370 ($5,400 - $5,030 = $370) would fall into the Donut Hole where you would get a 75% discount -- you pay $92.50 (25% of $370). The Donut Hole cost-sharing ($92.50) plus the Initial Coverage cost-sharing are added together for this one purchase.

Question: Will I exit the Donut Hole when I use an $1,800 drug?

Yes, sometime in month 5. If you continue to purchase the $1,800 drug each month, you would exit the Donut Hole sometime in month five (during your fifth drug purchase) when your true out of pocket costs (TrOOP) exceeds the annual 2024 TrOOP threshold of $8,000. After you exceed the $8,000 out-of-pocket limit, you will enter the Catastrophic Coverage portion of your Medicare Part D plan and you will pay nothing ($0) for formulary drug purchases for the remainder of the year.

Question: How can I calculate my annual drug costs?

You can use our Donut Hole calculator to get an estimate of when you will enter and exit the Donut Hole -- and your monthly costs as you move through your Medicare plan phases. (Please note we show the adjustment for the Donut Hole Discount following the monthly costs chart.)

See our FAQ for examples of the maximum Donut Hole Discount savings for other plan years.

Browse FAQ Categories

Pets are Family Too!

Use your drug discount card to save on medications for the entire family ‐ including your pets.

- No enrollment fee and no limits on usage

- Everyone in your household can use the same card, including your pets

Your drug discount card is available to you at no cost.

Q1 Quick Links

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service