Your retail drug cost counts toward reaching your plan's Initial Coverage Limit.

If you are using a brand-name formulary drug with a retail cost of $400 and paying only a $47 copay, the $400 retail drug value counts toward meeting your plan's Initial Coverage Limit.

Your Initial Coverage Limit (Donut Hole entry point) changes every year.

Since your plan's annual Initial Coverage Limit usually will change every year - so even if your Part D formulary prescriptions do not change - and the retail price of your prescriptions does not change - the point in time when you enter the Coverage Gap can change year-to-year:

- Entering the 2023 Donut Hole

In 2023, the standard Initial Coverage Limit (ICL) was $4,660 and if your 2023 Medicare prescription drug plan used the standard $4,660 ICL, you entered the Donut Hole sometime during 2023 if your average monthly retail drug costs were over $389.

- Entering the 2024 Donut Hole - the last year of the Donut Hole

In 2024, the standard Initial Coverage Limit (ICL) is $5,030 and if your 2024 Medicare prescription drug plan uses this standard $5,030 ICL, you would enter the Donut Hole sometime during 2024 if your average monthly retail drug costs are over $420.

- Important changes coming in 2025:

In 2025, the Inflation Reduction Act (IRA) of 2022 eliminates the Coverage Gap or Donut Hole and extends the Initial Coverage Limit until a person has spent $2,000 out-of-pocket for Part D formulary drugs. The $2,000 will represent the prescription drug maximum out-of-pocket spending limit (RxMOOP). The 2025 estimated total retail value of drugs you would need to purchase before reaching the RxMOOP of $2,000 is $6,230. Therefore, you will reach the RxMOOP of $2,000 at some time in 2025 if the retail value of your monthly Medicare Part D formulary drug costs is over $520 – and at that point, you will not have any additional costs for Part D formulary drugs for the remainder of the year.

Question: But I thought the Donut Hole went away?

Not exactly. Although we say that the Donut Hole is now "closed" since you receive a 75% discount on all formulary drugs if you enter the Donut Hole - it is possible that the cost of your formulary medications can increase, decrease, or stay the same once you are in the Donut Hole (Coverage Gap) - depending on your Medicare drug plan, your initial cost-sharing, and the drug's retail price.

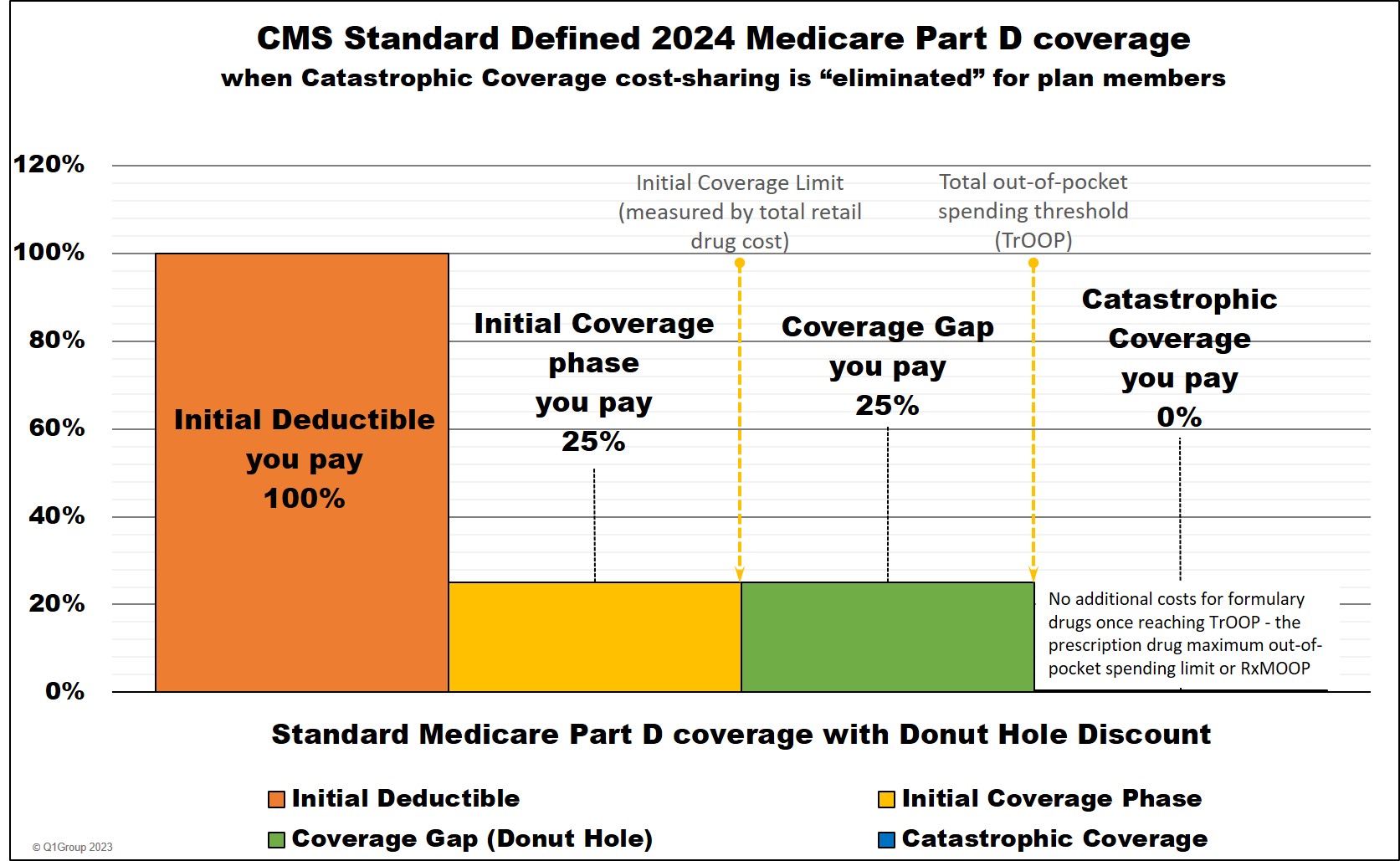

For example, if your Medicare Part D plan follows the standard Medicare Part D prescription drug plan, you will pay a fixed 25% cost-sharing in the Initial Coverage phase and then, if you enter the Donut Hole, you will continue to pay the same 25% coinsurance for all formulary drugs purchased - and since there is no change in coverage between being your 25% Initial Coverage phase and 25% Coverage Gap - the Donut Hole appears to be closed (see the diagram below).

However, if you usually pay a fixed copay for your drugs (for example, $47 for a $300 drug), you will pay 25% of $300 if you enter the Donut Hole or $75. So, you would pay more in the Donut Hole ($75) than you did in your Initial Coverage phase ($47).

You can click on our FAQ "Did the Coverage Gap or Donut Hole just close up and go away?" to read more.

The following is a graphic showing how the Donut Hole appears to be closed when you pay a flat 25% of retail during the Initial Coverage phase and the Coverage Gap.

Remember: 2024 is truly the last year for the Donut Hole. Beginning with plan year 2025, the Donut Hole will not exist.

Review: Your Part D drug plan coverage

As noted, you will enter your Medicare Part D prescription drug plan's Donut Hole or Coverage Gap if the total retail value of your formulary prescription purchases exceeds your plan's Initial Coverage Limit -- and most 2024 Medicare Part D plans (PDPs or MAPDs) use the standard Initial Coverage Limit of $5,030. You can read more in our article: "Understanding the 2024 Medicare Part D Donut Hole".

Example: What if you use only one formulary drug per month with a $495 retail value

If you use only one brand name, Tier 3 formulary medication that has a retail cost of $495 and you pay only a $47 copay with your Medicare Part D plan, your Medicare plan will pay the remaining $448 ($495 - $47), but the total retail cost of $495 counts toward meeting your $5,030 Initial Coverage Limit (in 2024).

So if your average monthly retail drug costs are $495, you will enter the 2024 Donut Hole or Coverage Gap in October - and your Donut Hole coverage cost will increase to $124 per month (based on the 75% Donut Hole discount) instead of the $47 copayment. See our chart below to estimate when you enter the Donut Hole based on your retail drug costs.

Question: How does "Retail Drug Cost" compare to "Your actual out-of-pocket drug cost"

Negotiated retail drug costs are not what you actually spend out-of-pocket for your prescriptions. Instead, retail cost is what you spend plus what your Medicare Part D plan pays (or others pay on your behalf). Using the example above, your plan's negotiated retail price is $495, but your actual out-of-pocket drug cost is a $47 copay.

Unfortunately, your Medicare plan's monthly Explanation of Benefits (EOB) letter does not state "Retail Drug Cost", but instead, your EOB will show two different columns with: "Plan Paid" and "You Paid" - when these two columns are added together, the sum is your Medicare drug plan's negotiated retail drug cost.

Review: "Lesser-of" rule used when your plan's cost-sharing is more than the drug's retail price

If the retail price of your formulary medication is less than your copayment, you will pay the retail price and not the higher copayment - based on the "lesser of" rule (you always pay the lesser of the retail cost or copay).

For example, if you are purchasing a Tier 3 generic medication with a $40 retail cost and the copay is $47, you will pay the $40 retail cost - and not the higher $47 copay.

Bottom line: You never pay more than your Medicare plan's negotiated retail drug price.

Question: Where can you see retail drug price information?

Your Medicare plan should have an online tool that shows you the most current retail price information for your formulary drugs - you can call your plan for more information about retail drug prices. The Medicare Plan Finder (MyMedicare.gov) also shows the plan's retail drug prices. You can also telephone a Medicare representative (1-800-Medicare) for retail drug price information.

In addition, both

our Formulary Browser (showing all drugs

for a single Medicare plan) and our Q1Rx® Drug Finder (showing all Medicare

plans covering a single drug) include CMS formulary data and average retail pricing information.

Please note, the retail drug prices shown within the Formulary Browser and Q1Rx Drug Finder show (when available) the average retail price for a particular drug

across a Medicare drug plan's network pharmacies (preferred and

standard) within a specific Service Area (Zip, state, or multi-state

area). But remember, retail drug prices can change regularly, even

changing on a weekly-basis - and prices can vary pharmacy-to-pharmacy -

and drug prices can vary between your plan's standard and preferred

network pharmacies - and retail drug prices can even vary between your plan's preferred network pharmacies.

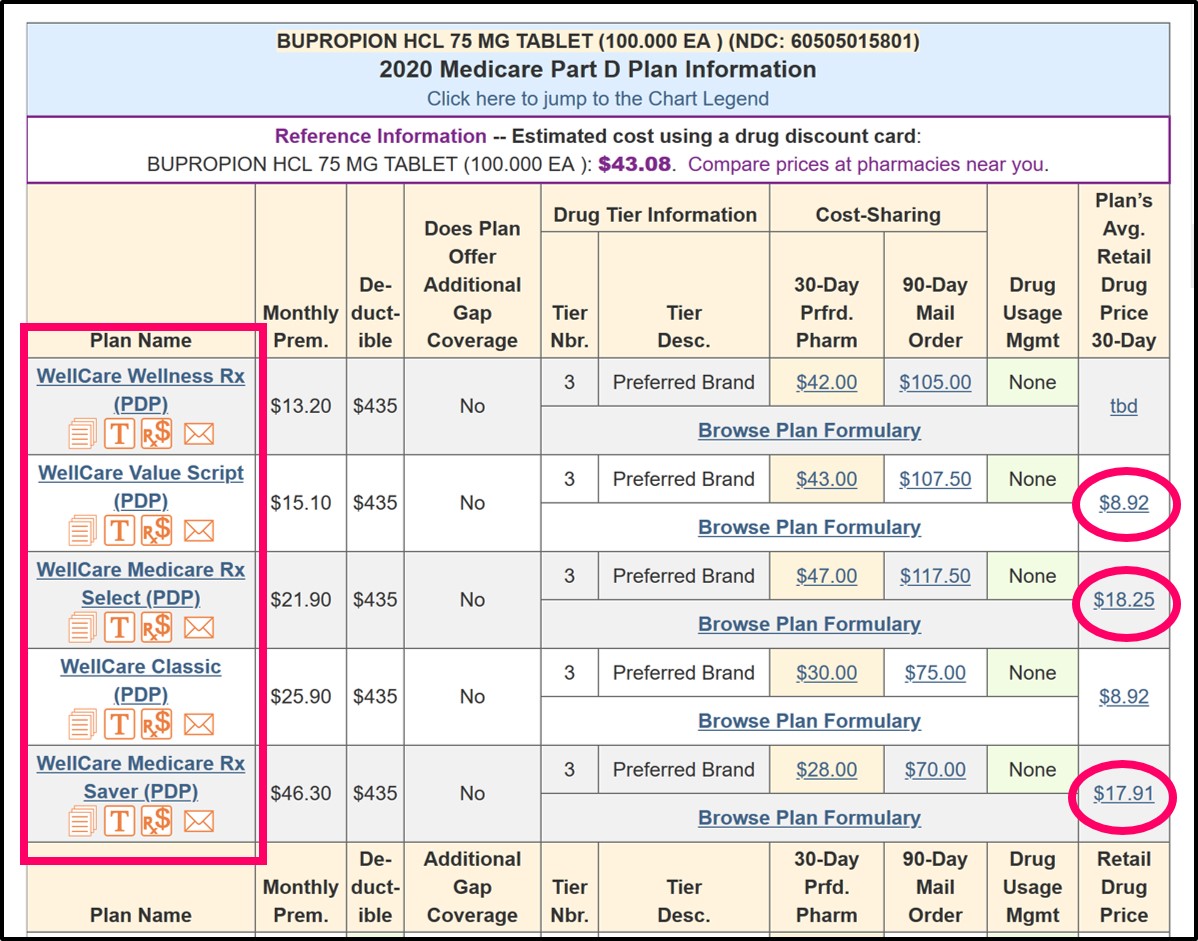

As an example, in the graphic below (Q1Rx.com/2020/FL/60505015801) you can see that several Medicare Part D plans offered by the same company (WellCare) have different average negotiated retail drug prices for the same drug (BUPROPION HCL 75 MG TABLET (100.000 EA) (NDC: 60505015801)) - the retail drug prices can then change week-to-week and pharmacy-to-pharmacy.

For more information, our Retail Drug Pricing Detail pages show the pricing history for each medication (when available). As noted, our retail drug pricing information is the average price across all pharmacies in a specific region and actual retail drug costs can vary slightly at your specific pharmacy.

Entering the 2024 Donut Hole as compared to the 2023 Donut Hole

The good news: If retail costs of your prescription have not

changed since 2023 (which is unlikely), the 2024 Donut Hole or Coverage Gap should start

just slightly later since the 2024 Initial Coverage Limit

($5,030) is slightly higher than the

2023 Initial Coverage Limit of $4,660.

In other words, you will be able to purchase slightly more prescriptions before entering the

2024 Donut Hole as compared to 2023.

Example of how entering the Donut Hole changes over the years.

If your average monthly retail medication costs were $400 in 2016,

you entered the 2016 Donut Hole in early-September 2016.

However, if your costs remained the same the next year,

you entered the 2017 Donut Hole sometime in early-October 2017.

Based on the same $400 average monthly retail drug cost,

you entered the 2018 and 2019 Donut Holes in mid-October

and you entered the 2020 Donut Hole early-November.

In 2021, you entered the Donut Hole slightly later in early-November and

in 2022 and 2023 you entered the Donut Hole in early- to mid-December.

And in 2024, if your monthly costs are $400 per month, you will NOT enter the Donut Hole.

And in 2025, there will be no more Donut Hole!

More good news: No Donut Hole for Medicare beneficiaries with Extra Help

If you receive Medicare Part D Extra Help or Low-Income Subsidy (LIS), then you will never enter the Donut Hole and the cost of your prescriptions will remain constant until you reach the Catastrophic Coverage portion of your Medicare Part D plan coverage where all Medicare beneficiaries pay nothing for their formulary prescriptions.

And if you are qualified for your state's Medicaid program, you are automatically qualified for Extra Help.

And more good news: Once any Medicare beneficiary enters the Catastrophic Coverage phase,

they will have no cost-sharing for the remainder of the year. Starting in 2024,

the Catastrophic Coverage phase will still exist, but plan members will not have any out-of-pocket costs for

formulary drugs after reaching the plan's $8,000 total out-of-pocket threshold

(TrOOP), thanks to the Inflation Reduction Act (IRA) of 2022.

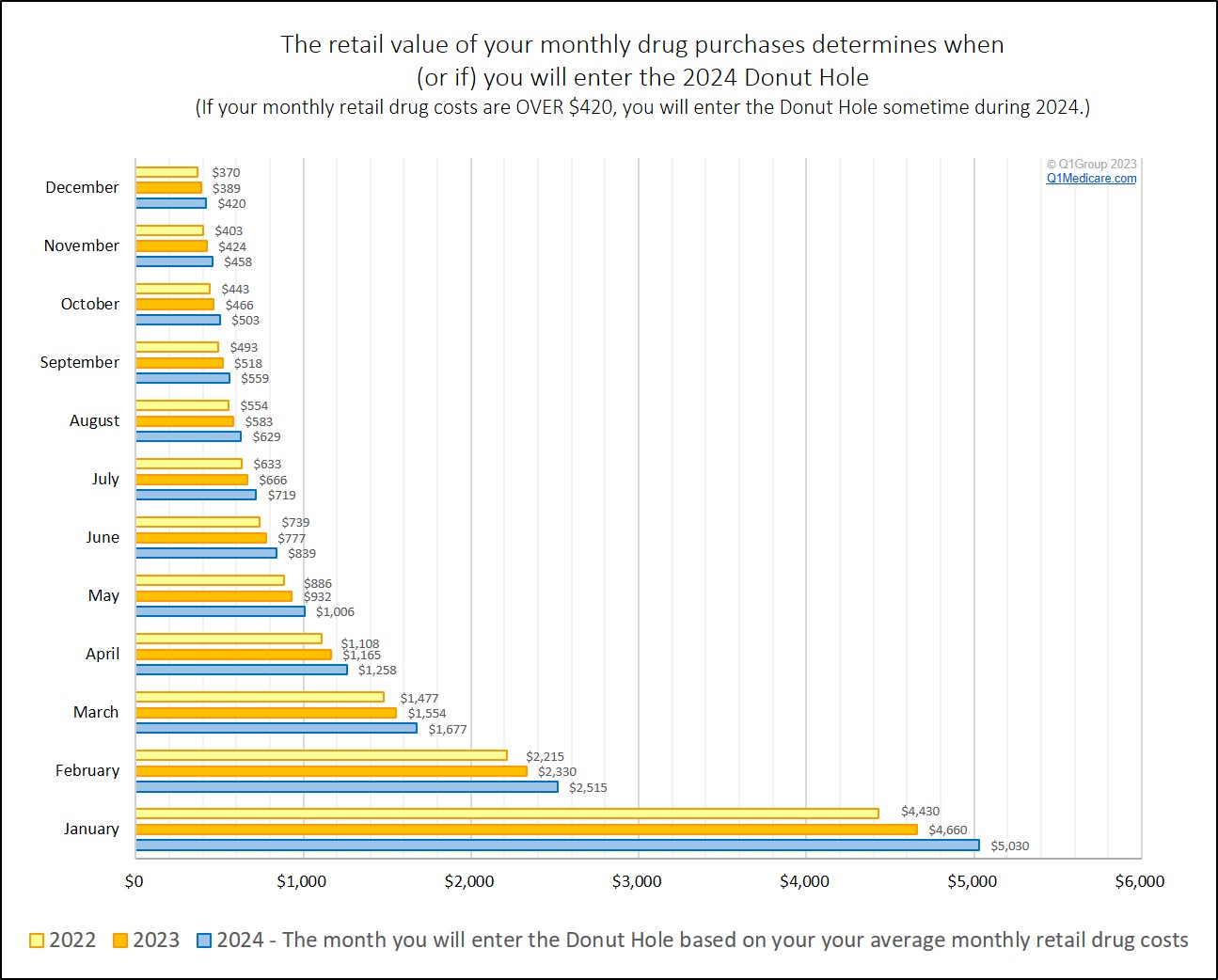

Question: If you are purchasing Medicare Part D drugs with a retail cost of over $420 per month, when will you enter the 2024 Donut Hole or Coverage Gap?

The chart below shows the average retail drug costs that would cause you to enter the

Coverage Gap or Donut Hole for any given month.

|

Minimum

Average Monthly Retail Drug Cost |

|||||

|---|---|---|---|---|---|

| Month you will enter

the Donut Hole |

If your 2024

monthly retail drug

costs are over . . . |

If your 2023

monthly retail drug

costs are over . . . |

If your 2022

monthly retail drug

costs are over . . . |

If your 2021

monthly retail drug

costs are over . . . |

If your 2020

monthly retail drug

costs are over . . . |

| January | $5,030 | $4,660 | $4,430 | $4,130 | $4,020 |

| February | $2,515 | $2,330 | $2,215 | $2,065 | $2,010 |

| March | $1,677 | $1,554 | $1,477 | $1,377 | $1,340 |

| April | $1,258 | $1,165 | $1,108 | $1,033 | $1,005 |

| May | $1,006 | $932 | $886 | $826 | $804 |

| June | $839 | $777 | $739 | $689 | $670 |

| July | $719 | $666 | $633 | $590 | $575 |

| August | $629 | $583 | $554 | $517 | $503 |

| September | $559 | $518 | $493 | $459 | $447 |

| October | $503 | $466 | $443 | $413 | $402 |

| November | $458 | $424 | $403 | $376 | $366 |

| December | $420 | $389 | $370 | $345 | $335 |

And here is how some of these retail drug costs would look in a chart . . .

Bottom line: If the retail cost of your medications averages over $420 each month -- and you are not eligible for Extra Help -- you will enter the Donut Hole sometime during 2024.

Related: Will you enter the 2024 Medicare Part D Coverage Gap or Donut Hole

Entering the Donut Hole and the Donut Hole Discount

If you are enter the Donut Hole, you will pay 25% of retail for brand drugs and 25% of retail for generic drugs.

Using our earlier example, if you are using a brand-name drug with a retail cost of $395, and you enter the Donut Hole, you would receive the brand name Donut Hole discount and pay 25% of retail or $99 (and so yes, even though considered "closed", coverage in the Donut Hole is costing you more than your $47 copay from your Initial Coverage Phase).

Estimating your Medicare Part D plan spending with our Donut Hole Calculator

You can also use our Donut Hole Calculator or PDP-Planner to get an idea of how you can budget for 2024 drug costs.

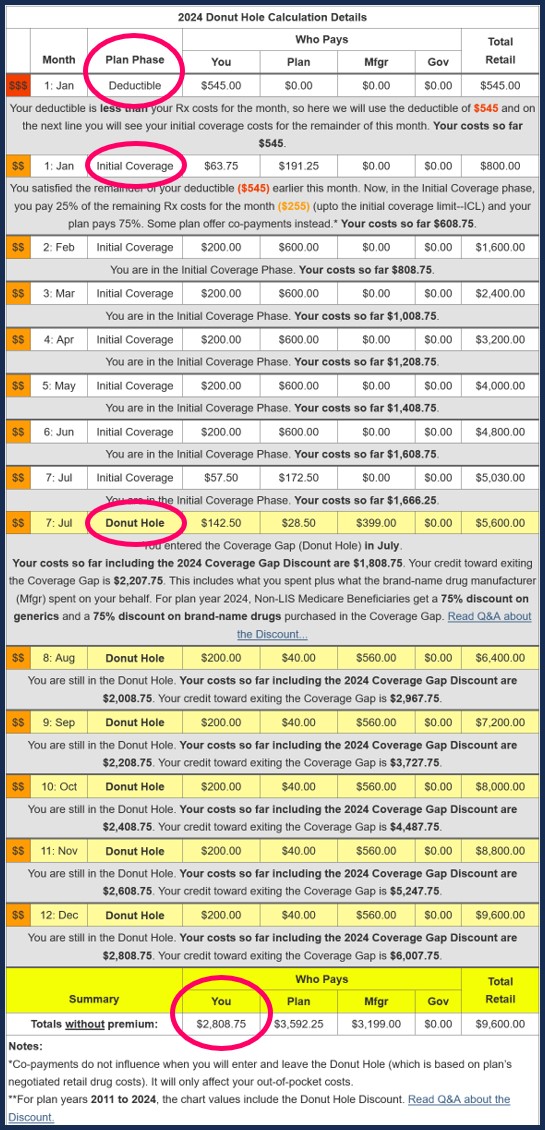

The following link shows an example of a person with retail brand-name drug costs totaling $800 per month: q1medicare.com/pdpplanner/2024/ex1 (as noted below, you can adjust the example and drug mix to estimate your actual out-of-pocket costs).

Spoiler Alert: In this 2024 example, if your average retail drug cost are $800 per month, and you use only brand-name drugs, you enter the 2024 Donut Hole in June, and do not exit into Catastrophic Coverage. Your out-of-pocket drug costs would be about $2,809 for the year.

If you wish, you can change the $800 value in our example to your own prescription spending - change the deductible (which is set at $0 Initial Deductible by default) - and choose your mix of generic or brand-name drugs) to see a preview of your own 2024 Medicare Part D drug coverage.

Still not sure what all these numbers mean to you? Click here and let us know.

- Will you enter the 2024 Medicare Part D Coverage Gap or Donut Hole

- Will you enter the 2023 Medicare Part D Coverage Gap or Donut Hole

- Will you enter the 2022 Medicare Part D Coverage Gap or Donut Hole

- Will you enter the 2021 Medicare Part D Donut Hole?

- Will you enter the 2020 Medicare Part D Donut Hole?

- Will I enter the 2019 Medicare Part D Coverage Gap or Donut Hole?

- Will I enter the 2018 Medicare Part D Coverage Gap or Donut Hole?

- Will you enter the 2017 Medicare Part D Donut Hole ... and if so, when?

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service