What is the Initial Deductible and How Does it Work?

The Initial Deductible phase is the first phase of your Medicare Part D prescription drug coverage. Typically during this phase of coverage, you are 100% responsible for your medication costs—up to the initial deductible.

For example, if your plan’s initial deductible is $545, you would be responsible for the first $545 of your prescription costs. If you have a Tier 3 medication with a $100 retail cost, you would pay 100% of the $100 until you spend $545.

The initial deductible is for a calendar year, so on January 1st of each year, when your new Medicare Part D plan coverage takes effect, you are once again in the Initial Deductible phase.

If you change Medicare prescription drug plans during the year, your year-to-date out-of-pocket costs will transfer to your new Medicare plan, so if you have already paid $545, you would not need to re-start your Medicare Part D plan coverage and pay a second Initial Deductible in your new plan.

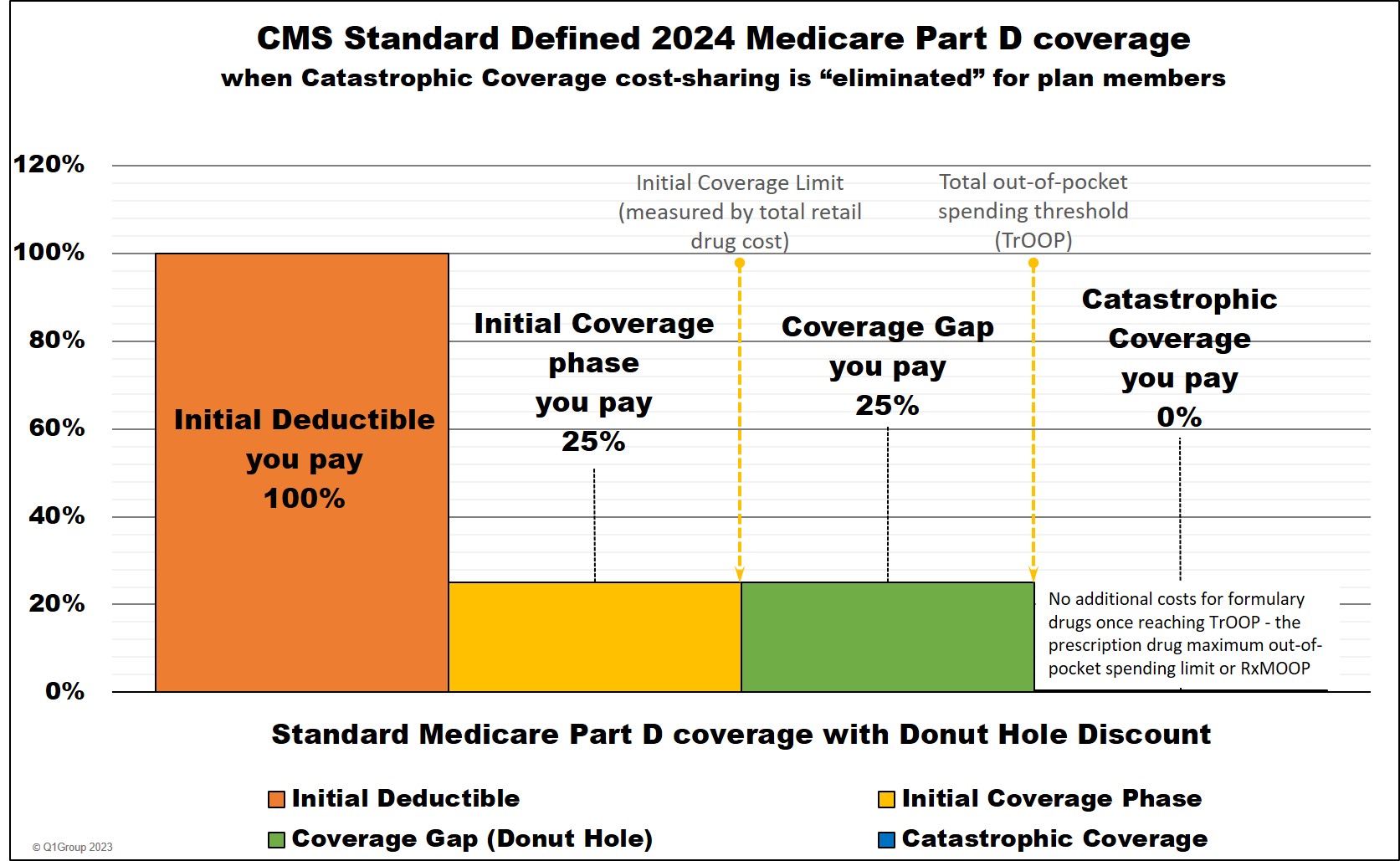

The CMS Standard Initial Deductible

Each year the Centers for Medicare and Medicaid Services (CMS) establishes the Medicare Part D standard initial deductible. The 2024 standard initial deductible set by CMS is $545. This figure is the maximum that Medicare Part D plans can set as the deductible for their prescription drug coverage. However, Medicare Part D plans are not required to use the CMS standard initial deductible.In fact, you may find that a Medicare Part D plan’s deductible:

- may be lower than the CMS standard deductible, but never higher,

- can be $0. These plans are also known as providing first dollar coverage,

- can exclude drugs on chosen formulary tiers.

When drug tiers are excluded from the Initial Deductible

Some Medicare Part D plans exclude lower costing generic drug tiers from the deductible (such as Tier 1 and Tier 2 drugs). This means that if you are in your plan’s initial deductible phase and you purchase a Tier 1 preferred generic drug with a retail cost of $8 and a copay of $1, you will pay the $1 copay. However, if you are in the initial deductible and buy a Tier 3 preferred brand-name drug with a retail cost of $75 and a copay of $30, you will pay the $75 retail cost, because this drug tier (Tier 3) is not excluded from the deductible.Some examples of how the Initial Deductible works

In this example, it is January and we just started a new Medicare Part D plan year.

You would pay $430 in cost-sharing (the full retail price) and you would then have a remaining Initial Deductible balance of $115 ($545 - $430).

If your next purchase is another Tier 3 drug with a $143

retail cost and a copay of $47, you would first cover the $115 balance of your deductible (from Example 1),

and then have $28 remaining ($143 retail price for this purchase - $115

deductible balance from the previous purchase). The $28 would

"straddle" into the second

phase of your Medicare Part D coverage

(Initial Coverage Phase)

where you have a $47 copay for this Tier 3.

Your cost-sharing would calculate to $162 the remainder of the deductible ($115)

plus the copay for the initial coverage phase ($47), however . . .

Since you never pay more than retail

($143), your cost-sharing would be $143 rather than $162 because the retail price

($143) is less than the calculated cost-sharing of $162. Your next drug purchases will be completely in the

Initial Coverage phase (your second phase of coverage) - and you will only pay your copay.

If you have a $115 balance remaining in your Initial Deductible (from Example 1) and

you purchase a $370 Tier 3 drug that has a $47 copay, you would first cover the $115 balance to meet your $545 Initial Deductible. The remaining amount of the retail price $255.

- $115 (left over in Deductible from the last purchase)

$255 (goes into the Initial Coverage phase)

This $255 would carry over to the Initial Coverage phase. So this one purchase would

"straddle" two phases of coverage. In this example, you have a $47 copay in the initial coverage phase.

We would calculate your cost-sharing as $162 — the remainder of the deductible ($115) plus the copay for the initial coverage phase ($47).

As you know from the last example, you never pay more than retail. But in this example, your calculated copay ($162) is less than the retail cost of your medication ($370), so your cost-sharing would be $162 ($115 + $47) for this purchase. Again, the $47 is the copay on the $255 remaining retail balance of the $370 drug purchase that falls or

"straddles" from your Initial Deductible phase into the Initial Coverage phase.

Your next drug purchases will be completely in the Initial Coverage phase (your second phase of coverage) — and you will only pay your copay.

Some Medicare Part D plans

exclude Tier 1 and Tier 2 drugs from the plan's Initial Deductible and these low-costing drugs are not impacted by your Initial Deductible and have

immediate coverage as if you were in your plan’s Initial Coverage phase.

So, if you have a $545 standard deductible with Tier 1 and Tier 2 drugs excluded from the deductible, and you purchase a

Tier 2 generic drug

that has a retail price of $22 (with a copay of $3) – you pay only the $3 copay and your $545 deductible is not affected. You can

click here to read more about Tier 1 and Tier 2 exclusions.

Since you have not met your $545 deductible, your first Tier 3 drug purchase should cost you $560 and straddle the

Initial Deductible and Initial Coverage phases.

Your cost-sharing would be calculated by first covering the $545 Initial Deductible, the remaining $15 portion

of the retail cost ($560 - $545)

would carry over to your Initial Coverage phase where you have a $40 copay, making your calculated cost-sharing for this purchase

$585 ($545 + $40).

This would mean that your cost-sharing would calculate to $585 the deductible ($545) plus the copay

for the initial coverage phase ($40). But . . .

Since you never pay more than the

drug plan’s retail cost ($560), and your

cost-sharing would be $585, which is higher than the drug’s retail cost, you pay the retail cost ($560).

When you make your next Tier 3 drug purchase, you would be in the Initial Coverage phase and pay only the $40 copay.

Additional articles on the Initial Deductible

Below are additional links from our news articles and frequently asked questions (FAQ) about the Medicare Part D Initial Deductible phase of coverage.- Slightly fewer 2024 MAPDs have a $0 premium and $0 drug deductible ($0/$0 plans) and fewer $0/$0 plans will refund a portion of your Part B premium.

- 85% of stand-alone 2024 Medicare Part D plans have an initial deductible.

- If I enroll in a Medicare prescription drug plan that has an initial deductible, will the deductible impact when I go into the Donut Hole?

- If I use an SEP to change my Medicare prescription drug plan during the year, will my initial deductible transfer to the new Part D plan?

- I am supposed to receive Extra Help so why does my Medicare Part D coverage have an initial deductible?

- Can I use a Drug Discount Card instead of my Medicare Part D plan if I only take low-cost generics and never leave my drug plan's Initial Deductible?

- No enrollment fee and no limits on usage

- Everyone in your household can use the same card, including your pets

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service