Example #1: If you have an initial deductible of $545 and you purchase a Tier 3 drug with a $665 retail value, you would first pay $545 to meet the initial deductible, then you would have a balance of $120 ($665 - $545) that would "straddle" or carry into your next coverage phase (the Initial Coverage Phase) where you have a $47 copay on Tier 3 drugs. So you would pay an additional $47 copay for the $120 balance that "straddled" into the second phase of coverage.

Your total cost for the $660 drug would be $545 + $47 = $592.

Straddle Claims and "Lessor-of Logic"

The cost of a drug purchase that crosses two or more parts of your Medicare Part D plan coverage is calculated using a combination of retail drug cost, copayments,and Donut Hole Discounts - but no matter what the calculation, you will never pay more than your plan's negotiated retail drug price (you will pay the "less-of" of the retail drug cost or the cost-sharing).

Example #2: Changing the Example #1 slightly, if you have an initial deductible of $545 and you

purchase a Tier 3 drug with a $550 retail value, you would first pay

$545 to meet the initial deductible, then you would have a balance of

$5 ($550 - $545) that would "straddle" or carry into your next

coverage phase (the Initial Coverage Phase) where you have a $47 copay

on Tier 3 drugs.

But, you would not pay an additional $47 copay for the $5

balance that "straddled" into the second phase of coverage - because your coverage cost would then be higher than the drug's retail cost. Instead, you would pay no more than the $550 retail drug price or ($545 + $5).

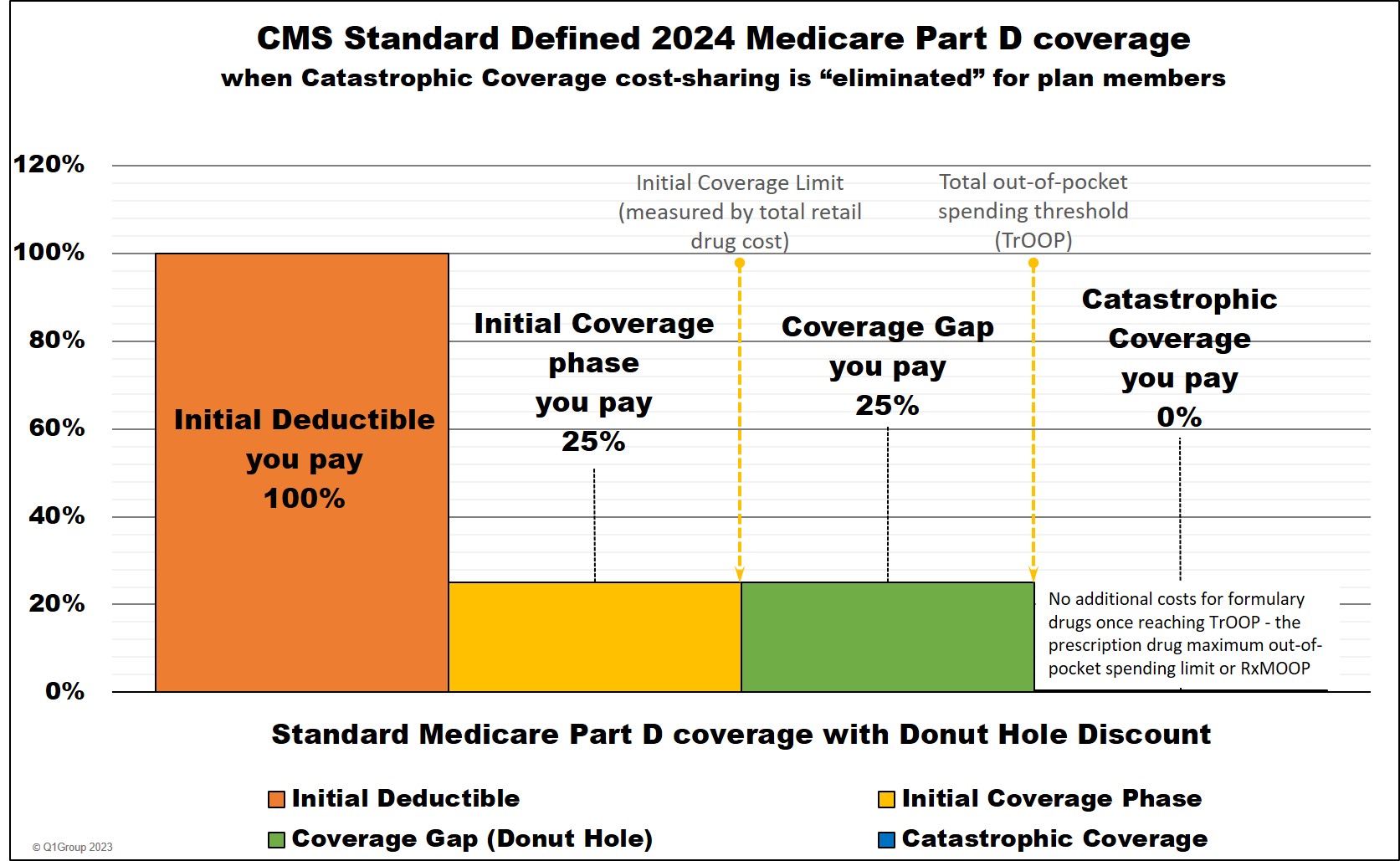

A quick review of your Medicare Part D plan coverage

Remember that your Medicare prescription drug plan has four (4) phases or parts, just like other insurance:

- (1) Initial Deductible phase - you pay 100% of your prescription purchases (unless you are enrolled in a Medicare plan with a $0 deductible, then you begin in the next part of coverage - or if your Medicare Part D plan excludes Tier 1 and Tier 2 drugs from the deductible, your deductible would only be applied to all other drugs). The standard Initial Deductible can change every year and the 2024 standard deductible (adopted by many Medicare Part D plans) is $545 ($590 in 2025).

- (2) Initial Coverage phase - you share the negotiated retail cost of your prescription purchases with your plan either as a coinsurance percentage (for instance, you pay 25% of retail) or as a fixed copayment (for instance, you pay a $30 copay for your Tier 3 formulary medication). When you have purchased covered medications with a retail cost of over your plan's Initial Coverage Limit (ICL), you will leave the Initial Coverage Phase (the standard 2024 ICL is $5,030) so when the retail value of drug purchases exceeds the ICL - you enter the Coverage Gap or Donut Hole. As a reminder, the Initial Coverage phase is not measured on what you pay, but the retail value of the formulary drug purchases.

- (3) Coverage Gap or Donut Hole phase - the Donut Hole Discount began in 2011 and is applied to all formulary purchases in the Donut Hole. (Also, some Medicare Part D drug plans provide supplemental coverage thought the Donut Hole or Coverage Gap - so members may not even notice that they have exceeded their Initial Coverage Limit, left the Initial Coverage Phase, and entered the Donut Hole for more information, be sure to refer to your Explanation of Benefits letter that your Medicare plan sent you.) Starting in 2020, you will receive a 75% discount on all formulary medications (generic and brand) while in the Donut Hole.

- (4) Catastrophic Coverage phase - after spending a certain amount out-of-pocket for your medications ($8,000 in 2024 and $2,000 in 2025), you enter the Catastrophic Coverage phase.

Beginning with plan year 2024, the Inflation Reduction Act (IRA) of 2022 eliminates beneficiary cost-sharing once your TrOOP reaches the established maximum cap on out-of-pocket spending for Part D formulary drugs (RxMOOP) $8,000 in 2024 and $2,000 in 2025.

Four Common Types of Straddle Claims

Depending on your Medicare Part D prescription drug plan benefit design (that is, whether your Medicare Part D prescription drug plan has an Initial Deductible or whether your plan provides some additional coverage in the Donut Hole), Straddle Claims usually occur in four situations - when prescription drug purchase claims cross:

(1) From the Initial Deductible phase into the Initial Coverage phase where coinsurance applies or the Initial Coverage phase where a copayment percentage structure applies. In this first case, you will pay the portion of the retail purchase price that satisfies the Initial Deductible and then the remainder of the retail cost will be charged some portion of cost-sharing in the Initial Coverage phase - where the total of the two charges does not exceed the drug's retail price.

As an example provided by Medicare, if a person was enrolled into a Medicare Part D plan with an initial deductible of $405 and their total covered retail drug purchases up to this time were $355 and now this same person just purchased covered prescription drugs with a negotiated retail price of $90.

Of that $90 retail price, $50 would falls at or below the $405 Initial Deductible limit, where the Medicare beneficiary is responsible for 100% of their prescription costs. So the person pays 100% of the first $50 plus the remaining $40 falls into the Initial Coverage phase, where the beneficiary pays a cost-sharing of 25% coinsurance (or $10) and this person's Medicare Part D prescription drug plan pays 75% [of the retail drug price]. [in the end], the person pays a total of $50 + $10 = $60 and not the full negotiated retail price of $90.

(2) From the Initial Coverage phase (or when the Initial Coverage Limit (ICL) is exceeded) during which a copayment or coinsurance applies and into the Coverage Gap (or Donut Hole) phase where coinsurance or (as of 2011) the Donut Hole discount applies.

(3) From the Coverage Gap or Donut Hole phase where coinsurance applies into the Catastrophic Coverage phase in which no ($0) copayment or coinsurance will apply (starting in 2024, there is no cost-sharing for formulary drugs once reaching Catastrophic Coverage).

(4) Finally, it is possible to straddle more than one part of your Part D coverage with a single, expensive drug purchase.

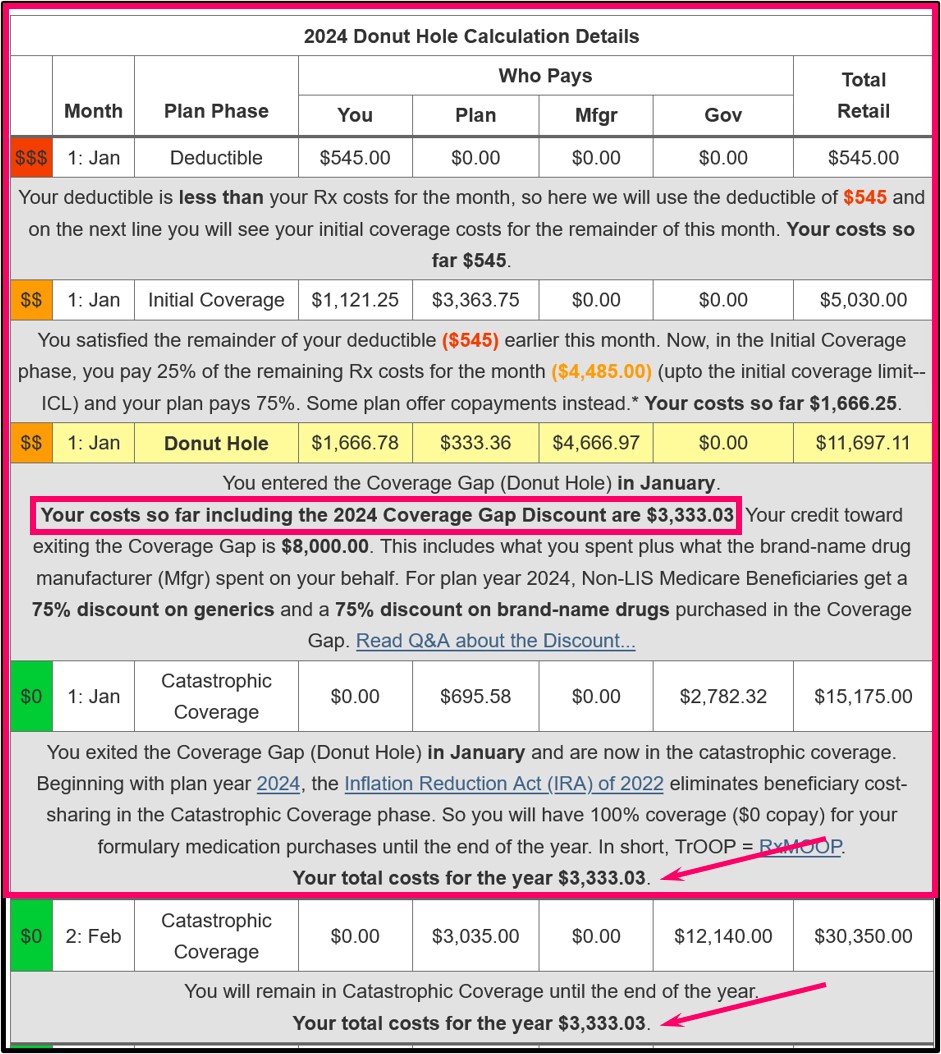

For example, what would a person pay when their first formulary drug purchase of the plan year was a $15,175 Tier 5 specialty drug and their plan has a standard $545 Initial Deductible?

Around $3,333. If you are using any brand-name medication with a retail cost over $12,051, having a 25% cost-sharing, you will move through (or straddle) all four phases of your drug coverage with a single purchase: (1) You will satisfy your $545 deductible, (2) enter and exit your Initial Coverage phase, (3) then enter and exit the Coverage Gap, and (4) finish in the Catastrophic Coverage phase (where, starting in 2024, you will have $0 cost-sharing).

The total retail drug cost of your first $15,175 purchase would be around $3,333 calculated as: $545 deductible + $1,121 in initial coverage phase + $1,667 in the Coverage Gap + $0 in the Catastrophic Coverage phase. (Again, once reaching the 2024 Catastrophic Coverage phase, you will have no cost-sharing ($0) for formulary drugs through the end of the year.)

Tip: To help you estimate your own out-of-pocket drug costs, you can use our PDP-Planner or out-of-pocket spending calculator – in this $15,175 example, you can enter a $545 deductible and choose 100% brand-name drugs and this will show you the costs in each Part D plan phase throughout the year - in this example, you can see that your out-of-pocket spending stops at $3,333 for the year.

Sources include:

The Center for Medicare and Medicaid Services, with clarifications, examples, and emphasis added)

https://www.cms.gov/Medicare/Prescription-Drug-Coverage/PrescriptionDrugCovContra/ Downloads/Final-Straddle-Claims-QA-4-26-07.pdf

- No enrollment fee and no limits on usage

- Everyone in your household can use the same card, including your pets

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service