Is there a difference between a Medicare Part D prescription drug plan (PDP) and a Medicare Advantage plan (MA/MAPD)?

Yes. A stand-alone Medicare Part D prescription drug plan (or PDP) only provides out-patient prescription drug coverage.

However, a Medicare Advantage plans provide coverage for your Original Medicare Part A (in-patient and hospitalization) and Medicare Part B (out-patient and doctor visits) - plus some Medicare Advantage plans may provide additional benefits like optical or eyeglass coverage, hearing aid coverage, fitness coverage (such as Silver Sneakers), OTC drug coverage, and dental coverage - plus Medicare Advantage plans can include Medicare Part D prescription drug coverage (MAPDs).

So, this means Medicare Advantage plans can be separated into two general groups:

(1) Medicare Advantage plans with prescription drug coverage (MAPDs) and

(2) Medicare Advantage plans without prescription drug coverage (MAs).

A Medicare Advantage plan (MA or MAPD) is also known as a Medicare Part C plan.

Drug Coverage and Pharmacy Participation and Healthcare Provider Networks

When choosing a stand-alone PDP, potential plan members need to ensure that their medications are covered in the plan's formulary and that their local pharmacies are included in the Medicare Part D prescription drug plan network.

As can be imagined, the selection of a Medicare Advantage plan (MAPD or MA) is more complicated than selecting a stand-alone Medicare Part D plan. When choosing a Medicare Advantage plan that includes prescriptions (MAPD), the potential plan member must also ensure that their prescriptions are covered by the plan and that their local pharmacies are part of the Part D plan network -- and Medicare beneficiaries must determine whether their favorite physicians or specialists and hospitals are included with the Medicare Advantage plan's healthcare network.

Requirements for Enrollment: Medicare Eligibility

To enroll into a Medicare Part D prescription drug plan, you must be eligible for either Medicare Part A and/or Medicare Part B coverage. Monthly Medicare Part D premiums are paid in addition to your Medicare Part A (if any) and/or Part B premiums.

To enroll into a Medicare Advantage plan (MA or MAPD), you must have both Medicare Part A and Medicare Part B coverage.

Medicare Advantage Plans are operated by private insurance carrier and compensated by the federal government. Monthly Medicare Advantage premiums are also paid in addition to your Medicare Part A and Medicare Part B premiums. As noted below, some Medicare Advantage plans have a $0 monthly premium - and a few Medicare Advantage Plans not only have a $0 premium, but you actually get a portion of your Medicare Part B premium rebated or paid-back.

Joining a Medicare plan in your Service Area

The only location-related requirement for joining a Medicare Part D or Medicare Advantage plan is that you live in (or be a permanent resident of) the Medicare plan's service area.

A Medicare Part D plan's service area is either a state or multi-state region (for example, both Pennsylvania and West Virginia are in the same CMS Region 6 and both states offer the same stand-alone Medicare Part D plans). You can view all of the stand-alone Medicare Part D plans in your area using our PDP-Finder tool:

PDP-Finder.com (begin by choosing your state abbreviation).

Here is an example link showing all Medicare Part D plans in Florida: PDP-Finder.com/FL

A Medicare Advantage plan's service area is much smaller than a Medicare Part D plan's service area and usually is a ZIP Code region or county. In some very populated areas (such as Los Angeles or New York City), a Medicare Advantage plan's service area may be a portion of the large city. You can view all of the Medicare Advantage plans in your area using our Medicare Advantage Plan Finder (or MA-Finder.com).

As an example, here are all the counties in Florida with links to the available Medicare Advantage plans: MA-Finder.com/FL

If you are using our online Medicare Advantage plan search tool at MA-Finder.com - just enter your ZIP and "Click to Find Plans". Here is an example of all Medicare Advantage plans in Summit County, Ohio using the ZIP 44319: MA-Finder.com/44319

However, a Medicare Advantage plans provide coverage for your Original Medicare Part A (in-patient and hospitalization) and Medicare Part B (out-patient and doctor visits) - plus some Medicare Advantage plans may provide additional benefits like optical or eyeglass coverage, hearing aid coverage, fitness coverage (such as Silver Sneakers), OTC drug coverage, and dental coverage - plus Medicare Advantage plans can include Medicare Part D prescription drug coverage (MAPDs).

So, this means Medicare Advantage plans can be separated into two general groups:

(1) Medicare Advantage plans with prescription drug coverage (MAPDs) and

(2) Medicare Advantage plans without prescription drug coverage (MAs).

A Medicare Advantage plan (MA or MAPD) is also known as a Medicare Part C plan.

Drug Coverage and Pharmacy Participation and Healthcare Provider Networks

When choosing a stand-alone PDP, potential plan members need to ensure that their medications are covered in the plan's formulary and that their local pharmacies are included in the Medicare Part D prescription drug plan network.

As can be imagined, the selection of a Medicare Advantage plan (MAPD or MA) is more complicated than selecting a stand-alone Medicare Part D plan. When choosing a Medicare Advantage plan that includes prescriptions (MAPD), the potential plan member must also ensure that their prescriptions are covered by the plan and that their local pharmacies are part of the Part D plan network -- and Medicare beneficiaries must determine whether their favorite physicians or specialists and hospitals are included with the Medicare Advantage plan's healthcare network.

Requirements for Enrollment: Medicare Eligibility

To enroll into a Medicare Part D prescription drug plan, you must be eligible for either Medicare Part A and/or Medicare Part B coverage. Monthly Medicare Part D premiums are paid in addition to your Medicare Part A (if any) and/or Part B premiums.

To enroll into a Medicare Advantage plan (MA or MAPD), you must have both Medicare Part A and Medicare Part B coverage.

Medicare Advantage Plans are operated by private insurance carrier and compensated by the federal government. Monthly Medicare Advantage premiums are also paid in addition to your Medicare Part A and Medicare Part B premiums. As noted below, some Medicare Advantage plans have a $0 monthly premium - and a few Medicare Advantage Plans not only have a $0 premium, but you actually get a portion of your Medicare Part B premium rebated or paid-back.

Joining a Medicare plan in your Service Area

The only location-related requirement for joining a Medicare Part D or Medicare Advantage plan is that you live in (or be a permanent resident of) the Medicare plan's service area.

A Medicare Part D plan's service area is either a state or multi-state region (for example, both Pennsylvania and West Virginia are in the same CMS Region 6 and both states offer the same stand-alone Medicare Part D plans). You can view all of the stand-alone Medicare Part D plans in your area using our PDP-Finder tool:

PDP-Finder.com (begin by choosing your state abbreviation).

Here is an example link showing all Medicare Part D plans in Florida: PDP-Finder.com/FL

A Medicare Advantage plan's service area is much smaller than a Medicare Part D plan's service area and usually is a ZIP Code region or county. In some very populated areas (such as Los Angeles or New York City), a Medicare Advantage plan's service area may be a portion of the large city. You can view all of the Medicare Advantage plans in your area using our Medicare Advantage Plan Finder (or MA-Finder.com).

As an example, here are all the counties in Florida with links to the available Medicare Advantage plans: MA-Finder.com/FL

If you are using our online Medicare Advantage plan search tool at MA-Finder.com - just enter your ZIP and "Click to Find Plans". Here is an example of all Medicare Advantage plans in Summit County, Ohio using the ZIP 44319: MA-Finder.com/44319

Health-related enrollment questions

There are no health-related questions when joining a stand-alone Medicare Part D prescription drug plan. In other words, a PDP is guarantee issue, no matter what your health or medical history.

Since 2021, there are also no health-related questions when joining a Medicare Advantage plan. From 2006 through 2020, the only Medicare Advantage plan health-related question is whether you suffer from End Stage Renal Disease (ESRD) or kidney failure.

However, if you are trying to join a Medicare Advantage Special Needs Plan (SNP) for a specific chronic health condition (such as Diabetes) or due to your low-income status, you are required to have the condition (or economic need) in order to join the SNP. For example, if you join a D-SNP, a Medicare Advantage Special Needs Plan designed for people qualified for both Medicare and Medicaid, you must be Medicaid eligible or you will be disenrolled from the D-SNP.

Also a Medicare Advantage Special Needs plan for Dual-Eligible Medicare/Medicaid beneficiaries (D-SNP) can exclude people who suffer from End-Stage Renal Disease (ESRD), even though, after 2021, people who suffer from ESRD are allowed to join any Medicare Advantage plan.

Key Point: Medicare Advantage plans may have a $0 premiums -- or a $0 premium and Medicare Part B rebate

Like the Medicare Part D prescription drug plans, the Medicare Advantage plans are administered by private insurance carrier and compensated partially by the Federal Government.

Because of low region medical costs, some Medicare Advantage plans do not charge a monthly premium (or have a $0 premium) and a few Medicare Advantage plans actually rebate a portion of your Medicare Part B payment back to you (sometimes called a Dividend plan or Part B "Give Back") - this means you do not pay any monthly premium and may actually get a portion of your Medicare Part D premium "rebated" back to you in the form of a dividend.

So, in some areas of the country, you may find a Medicare Advantage plan with drug coverage that actually pays you back (or returns a portion of your Part B premiums) for your Medicare Part A, Medicare Part B, and Medicare Part D coverage.

Key Point: A Maximum Limit on your Medical Spending

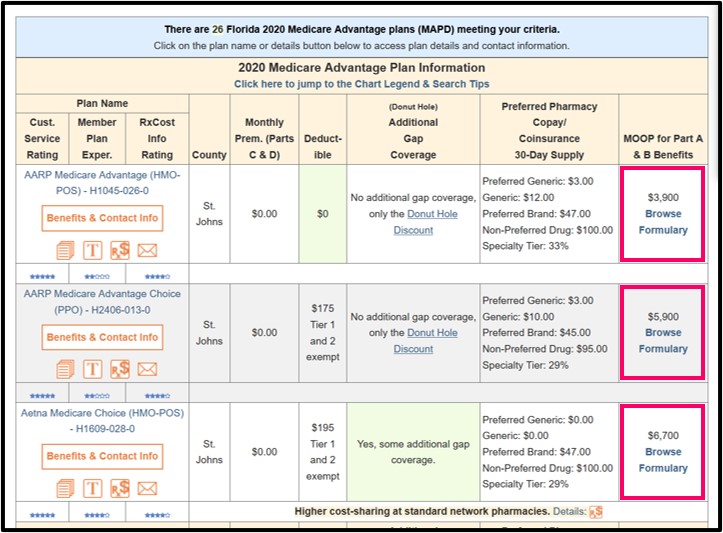

One of the biggest benefits of a Medicare Advantage plan is that there is a limit to your out-of-pocket medical spending that is established each year (or MOOP).

Please note: If you have Original Medicare Part A and Medicare Part B, there is no limit or cap to what you can pay each year for your Medicare Part A and Medicare Part B coverage. If you have very high medical expenses, you could have very high costs.

However, with your maximum out-of-pocket limit (MOOP), your private Medicare Advantage plan will limit your potential Medicare spending each year to some level such as $3,450, $5,000, $6,700, or $8,850 - depending on your chosen plan (note, the statutory maximum MOOP is $8,850 in 2024).

We show the MOOP levels for all Medicare Advantage plans in our MA-Finder Plan Finder tool.

Key Point: The Different Network Structures of a Medicare Advantage plan

Medicare Advantage plans (MA and MAPD) can be further defined by how the private insurance carriers choose to implement the Medicare Part A and Part B coverage.

Some Medicare Advantage plans are PPOs (Preferred Provider Organizations) - other MAs are organized as HMOs

(Health Management Organizations) - and still other MAs are set up as PFFSs (Private Fee for Service Organizations).

A number of key differences exist between the organization of a PPO, HMO, and PFFS. All three have some advantages and disadvantages.

A bit of Medicare History: The Private Market and Medicare Advantage Plans

From a very general perspective, Medicare Part D plans and Medicare Advantage plans were both introduced to take advantage of the competitive forces existing in a private market to help control the medical expenses. As noted in a (August 13, 2007) CMS Press Release:

An August 2015 Commonwealth Fund study entitled "Competition Among Medicare’s Private Health Plans: Does It Really Exist?", seriously question whether enough Medicare Advantage plans are offered to provide for a competitive environment. The study notes in its summary:

. . . and still a little more Medicare History: Marketing Compliance and the Medicare Advantage Plan

On another note, as some Q1Medicare site visitors have noticed, back in 2007, PFFS Medicare Advantage plans received a great deal of press due to allegations of unethical marketing activities. You can read more about that here: Plans Suspend PFFS Marketing; Plans adopt strict guidelines in response to deceptive marketing practices. Since this time, Medicare has increased enforcement and oversight of Medicare plans and such marketing practices are more limited today.

Additional Donut Hole Coverage?

Although somewhat rare today with the implementation of the Donut Hole discount, some stand-alone Medicare Part D plans or Medicare Advantage plans still offer some form of supplemental Donut Hole (or Doughnut Hole) coverage (for brand name and/or generic medications). We have Donut Hole coverage details in both our PDP-Finder and MA-Finder.

Medicare Advantage plans (MA and MAPD) can be further defined by how the private insurance carriers choose to implement the Medicare Part A and Part B coverage.

Some Medicare Advantage plans are PPOs (Preferred Provider Organizations) - other MAs are organized as HMOs

(Health Management Organizations) - and still other MAs are set up as PFFSs (Private Fee for Service Organizations).

A number of key differences exist between the organization of a PPO, HMO, and PFFS. All three have some advantages and disadvantages.

- HMOs (Health Management Organizations) - try to keep costs

down by having a more restrictive health care provider network (meaning

you will pay more when going outside the network).

- HMO-POS (an HMO Point of Service) - this HMO has a more

flexible network structure, allowing HMO members to use providers

outside of the network (usually at a higher cost) and may not count the

out-of-network costs toward the member's MOOP (or Maximum out-of-pocket

limit - see below).

- PPOs (Preferred Provider Organizations) - have a more flexible

healthcare provider network and usually have in-network and

out-of-network costs sharing.

- PFFS (Private Fee for Service Organizations) - have no

established network, and you can use any healthcare provide who accepts

the terms and conditions of the Medicare Advantage plan.

A bit of Medicare History: The Private Market and Medicare Advantage Plans

From a very general perspective, Medicare Part D plans and Medicare Advantage plans were both introduced to take advantage of the competitive forces existing in a private market to help control the medical expenses. As noted in a (August 13, 2007) CMS Press Release:

"[M]any beneficiaries have access to a Medicare Advantage plan with lower prescription drug premiums. It will be important for beneficiaries to compare their coverage options for 2008 based on overall cost, coverage, and convenience in order to select the plan that best meets their needs. MA-PD premiums continue to be lower than PDP premiums. On average, in 2007, the MA-PD premiums prior to rebates are about $7 lower than those for PDPs. In 2008, they will average $11 lower. The lower MA-PD bids and premiums reflect the effects of aggressive competition as well as lower costs resulting from better care coordination and drug benefit management techniques. In practice, many MA-PD plans also apply a portion of their rebates from Parts A and B to reduce their Part D premiums, in many cases to zero."

(CMS Press Release 08/13/2007) The entire CMS Press Release can be found as part of our article here.

An August 2015 Commonwealth Fund study entitled "Competition Among Medicare’s Private Health Plans: Does It Really Exist?", seriously question whether enough Medicare Advantage plans are offered to provide for a competitive environment. The study notes in its summary:

"Using a standard measure of market competition, our analysis finds that 97 percent of markets in U.S. counties are highly concentrated and therefore lacking in significant MA plan competition. Competition is considerably lower in rural counties than in urban ones. Even among the 100 counties with the greatest numbers of Medicare beneficiaries, 81 percent do not have competitive MA markets. Market power is concentrated among three nationwide insurance organizations in nearly two-thirds of those 100 counties." [emphasis added](source: https://www.commonwealthfund.org/ publications/issue-briefs/2015/aug/ competition-medicare-private-plans-does-it-exist)

. . . and still a little more Medicare History: Marketing Compliance and the Medicare Advantage Plan

On another note, as some Q1Medicare site visitors have noticed, back in 2007, PFFS Medicare Advantage plans received a great deal of press due to allegations of unethical marketing activities. You can read more about that here: Plans Suspend PFFS Marketing; Plans adopt strict guidelines in response to deceptive marketing practices. Since this time, Medicare has increased enforcement and oversight of Medicare plans and such marketing practices are more limited today.

Additional Donut Hole Coverage?

Although somewhat rare today with the implementation of the Donut Hole discount, some stand-alone Medicare Part D plans or Medicare Advantage plans still offer some form of supplemental Donut Hole (or Doughnut Hole) coverage (for brand name and/or generic medications). We have Donut Hole coverage details in both our PDP-Finder and MA-Finder.

Browse FAQ Categories

Q1 Quick Links

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2024 Medicare Part D plan Facts & Figures

- 2024 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2023/2024 Medicare Part D plan changes

- 2024 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2023 to 2024

- Drug Finder: 2024 Medicare Part D drug search

- Formulary Browser: View any 2024 Medicare plan's drug list

- 2024 Browse Drugs By Letter

- Guide to 2023/2024 Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2025 Medicare Part D Reminder Service