Medicare.gov - Tutorial - Compare Medicare Plans in Your List

You have two options back in Step 2 of 4 to get this far in the Medicare.gov Plan Finder without actually entering any prescription drugs. You could have chosen either: "I don’t want to add drugs now" or "I don’t take any drugs".

Both options in Plan Finder Step 2 of 4 skip the drug entry page and bring you directly to this Step 4 of 4.

However, the two similar options lead to different results with the "I don’t want to add drugs now" option adding in an estimated value of your medication costs even though no drugs were added.

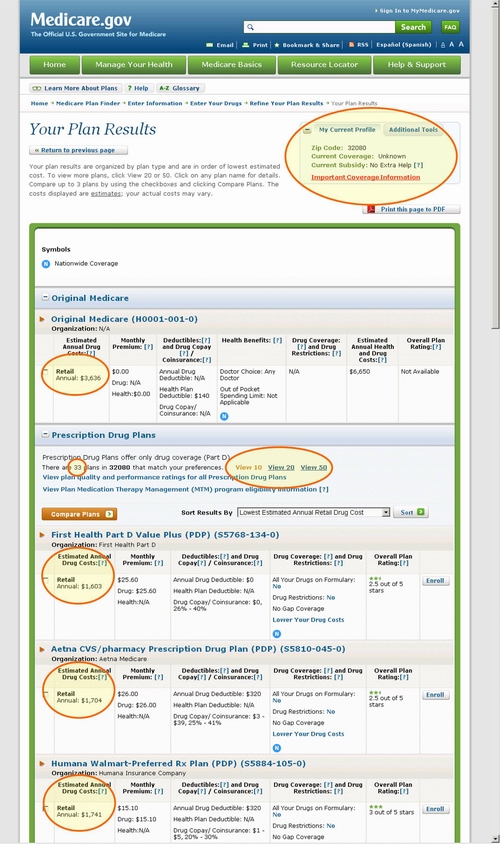

Back in 2012, if you chose not to enter any prescription drugs in Step 2 of 4 ("I don’t want to add drugs now") , the Plan Finder still estimated that your prescription drug cost for "Good" health would be $3,318 per year (the Plan Finder default health value is always "Good" ). In July of 2013, that estimated annual drug cost has increased to $3,636 for a person with "Good" health. When we changed our Health Status on the previous screen (left hand side, bottom of the options) to "Poor", our new estimated annual retail drug cost without any prescription drug coverage increased to $7,296. If we change the Health Status to "Excellent", our annual retail drug cost estimate would change to $1,656.

Since there is no better Health Status choice than "Excellent", people who take no prescriptions can either just ignore the annual Medicare drug cost estimate at this point or go back to Step 2 of 4 and click on "I don’t take any drugs" to get a better idea of having a Medicare Part D plan and not using any prescriptions.

If you chose "I don’t take any drugs" back in Step 2 of 4 "Enter Your Drugs", you will see the only annual cost for a Medicare Part D plan is simply the cost of the monthly premiums and no estimated drug cost is added. Therefore, if you just want the lowest prescription drug priced plan so you can avoid any late—enrollment premium penalty or just to have some form of drug insurance, you can quickly see the lowest annual costing plan available in your area by choosing "I don’t take any drugs" back in Plan Finder Step 2 of 4. If your health status changes, you can always go back to Step 2 of 4 and enter medications.

As we have mentioned, the Medicare.gov Plan Finder is constantly evolving and sometimes new features are added and sometimes old features are retired. You may notice that now the "Your Plan Results" page, the Plan Finder is a little sleeker without some of the older functions. For instance, in past versions of the Plan Finder, on this results page you could still change the type of Medicare plan you chose from the previous page (for instance, you could now say Medicare Advantage instead of Medicare of Medicare Part D plans). You may also notice that there is no longer a summary at the top of the page showing you the range of your possible annual prescription costs. (For instance, in our past version of this tutorial we showed an example using expensive medications that estimated the drug plan cost range from $4,950 to $105,300.)

There are a number of different costs associated with a Medicare Part D plan or a Medicare Advantage plan and they sometimes blur together when all presented at one time. Here are a few of the costs that we will see on this Your Plan Results page and when you go into more plan details.

You will notice other costs as well when reviewing Medicare prescription drug plans or Medicare Advantage plans, such as mail-order pharmacy costs (if available) that may be less than preferred network pharmacy costs —and the cost of health care coverage that is usually provided by Original Medicare Part A (in-patient care) and Medicare Part B (out-patient care).

The key at this point is to ensure that the Medicare prescription drug plans (or Medicare Advantage plans are sorted in order of estimated annual prescription costs (this assumes all cost including your monthly premium and initial deductible--if any). (Please notice that the Medicare plan sort order is controlled by a drop down box in the middle of the Plan Finder Your Plan Results page.) You can then look down the list to find a Medicare plan that most affordably covers your prescription medications or health coverage.

Just as medication retail drug pricing can change on the Medicare Plan Finder, Medicare Part D plans can add or remove medications throughout the plan year (starting in on March 1st). So it is possible that if you research plans and then return months later, you may find that the most affordable Medicare prescription drug plans have changed order. If you are already enrolled in a Medicare Part D plan, the plan must provide you with written notice about any drug list changes. But the notification is sent several months (60 days) before your coverage is actually affected and so the Medicare Plan Finder may not show that same advance notice until the plan’s drug list or formulary actually changes. This means, you may know that Medication XYZ is being dropped by your Medicare plan, but the Medicare Plan Finder may still show your plan covering XYZ until the medication is actually removed from the plan’s drug list.

One of interesting feature that the Medicare.gov site provides is a Plan Rating star system based on a number of Medicare plan quality factors. The ratings come from several sources including a sampling of experiences from people who have been enrolled in the particular Medicare plan and, like any sample of events, these Medicare findings may or may not correspond with your own experiences. We have found that often times a Medicare Plan that had a lower Medicare star rating one year will really work to raise the customer rating in the next years. When a new annual Open Enrollment Period begins, Medicare may not have yet gathered all of the necessary data and you may at some time find a screen message saying that the Medicare star or quality ratings data was not yet loaded by Medicare. No problem, the star ratings will return and you need to just check back to the Plan Finder at a later date.

As noted earlier, we consider the total annual drug cost to be one of the most important factors that folks should consider when choosing a Medicare Part D plan or Medicare Advantage plan. This figure is the total amount that you can be expected to pay for the whole year for your prescription drugs. The Estimated Annual Drug Costs include monthly premiums, initial deductible, and your portion of your actual prescription drug costs.

However, the annual cost alone is not all that is important when choosing a Medicare plan. Take a look at the plan’s Quality Star Rating. How have previous plan Members rated this plan? Take a look a the size of the Medicare plan’s formulary or drug list. All of your current medications may be covered, but paying a few dollars more per month for a plan with larger formulary may pay off if you are prescribed new medications after the start of the new plan year. If you are joining a Medicare Advantage plan, be sure that your local hospital, physicians and specialists are included in the plan’s network.

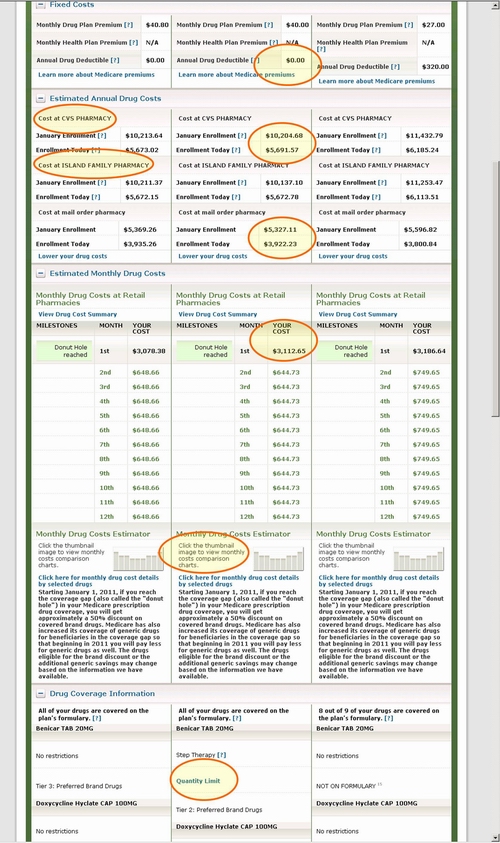

You may notice in our Plan Finder screen example that we chose two different pharmacies from the previous Step 3 of 4 and these two pharmacies have different Estimated Annual Costs for each of the three chosen plans we are comparing.

In the example screen, we see that one of the chosen plans has an Initial Deductible and the other two plans do not have a deductible.

If you look closer to plan cost details, you may notice that sometimes the Initial Deductible (again, this is the part of your Medicare

plan where you pay for everything yourself) does not always align neatly into the Plan Finder and there are two possible reasons for the

Total Cost figure to be over the initial deductible value:

(1) there are some medications that are on the Drug List that are not

included in the Medicare Part D plan formularies — and since they are not in the formulary the cost is not included toward the

Initial Deductible or the Initial Coverage Limit (before entering the Doughnut hole).

(2) Straddle Claims that break purchases

over several phases of a Medicare Part D plan. The Medicare.gov website shows costs for a total month and is not programmed to break

coverage periods within a month. In our Q1Medicare.com

Doughnut Hole Calculator,

e break the initial deductible into smaller portions and allow a person to go through multiple phases of coverage in a single month.

For example, a Medicare beneficiary could meet their initial deductible with the purchase of one expensive medication — well

before the end of the first month and with a very expensive drug like in our example screens (retail costs of around $10,000), the

person would go through all phases of the Medicare Part D plan and into Catastrophic Coverage with one purchase.

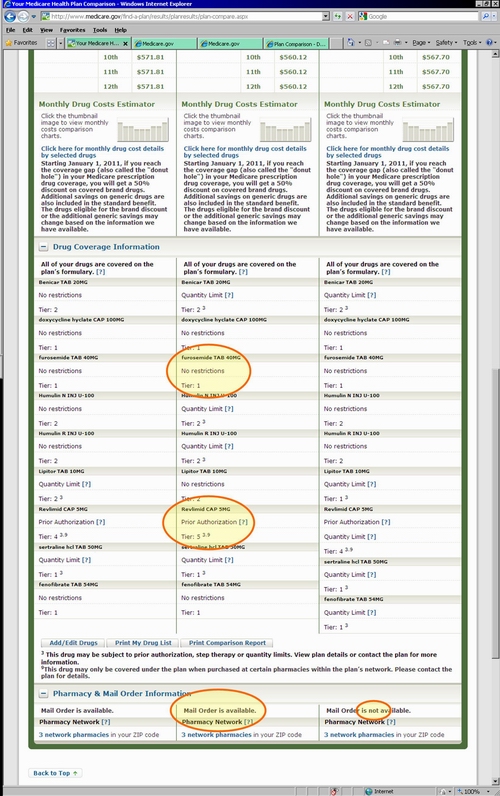

Nearing the bottom of the page is the "Drug Coverage Information" which shows the medications from the Drug List that are covered under the Medicare Part D plan formularies. Notice also that some medications are subject to usage management such as prior authorization, step therapy or quantity limits.

The Medicare Plan Finder has the Medicare Part D plan Quantity Limits online and summarized in a pop-up window for your entered medications. The quantity limits show you the amount of medication the chosen plan allows in a certain time limit. If you are using more than the quantity limit shown, you can always ask the Medicare Part D plan for a formulary exception or coverage determination so that your greater medication quantity will be covered or you can choose to join another Medicare plan that does not have this usage management restriction. Formulary exception requests can be denied, but if your request is denied, you can appeal the decision several times. If you wish to learn more about formulary exceptions or coverage determinations, you can click here for more information.

8am to 5pm MST

- Sign-up for our Medicare Part D Newsletter.

- PDP-Facts: 2025 Medicare Part D plan Facts & Figures

- 2025 PDP-Finder: Medicare Part D (Drug Only) Plan Finder

- PDP-Compare: 2024/2025 Medicare Part D plan changes

- 2025 MA-Finder: Medicare Advantage Plan Finder

- MA plan changes 2024 to 2025

- Drug Finder: 2025 Medicare Part D drug search

- Formulary Browser: View any 2025 Medicare plan's drug list

- 2025 Browse Drugs By Letter

- Guide to Consumer Mailings from CMS, Social Security and Plans

- Out-of-Pocket Cost Calculator

- Q1Medicare FAQs: Most Read and Newest Questions & Answers

- Q1Medicare News: Latest Articles

- 2026 Medicare Part D Reminder Service